Payment movers and shakers

Issue 373 | 19 August 2022

In this edition of the Payments:Unpacked Tracker 1 we see the impact on the volume and value of payments processed in the UK as we ‘live with Covid’ with the comparison now with similar conditions in the equivalent months in 2021 (when restrictions had been lifted at the end of Lockdown 3.0.)

Movers and shakers

The public perception of the term ‘movers and shakers’ began after the first performance of Sir Edward Elgar's popular choral work The Music Makers, at the Birmingham Festival in October 1912. The work is a setting of Arthur O'Shaughnessy's 1874 poem 'Ode', from his Music and Moonlight collection.

In that poem, which singles out poets and musicians as the bards that guide lay thinking, O'Shaughnessy coined the phrase 'movers and shakers'.

In this monthly payments statistics round up it is clear that Faster Payments remains the key payment rails ‘mover and shaker’!

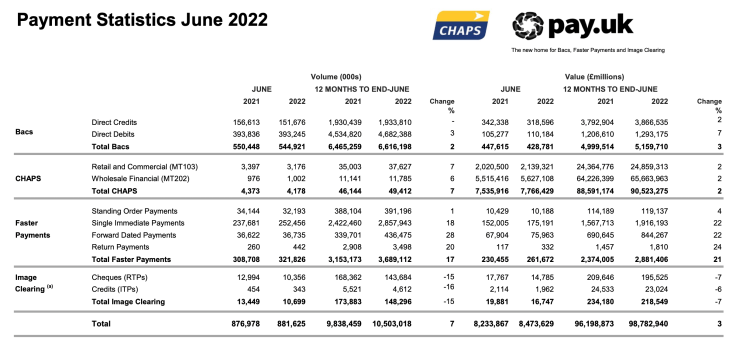

Bacs Direct Debit and Direct Credit

In the 12 months to the end of June 2022 we see that:

Bacs Direct Credit volumes have increased by 0% (12 months to May increased by 1%)

Bacs Direct Debit volumes have increased by 3% (12 months to May increased by 4%)

Total Bacs volumes have increased by 2% (12 months to May increased by 3%)

Bacs Direct Credit values have increased by 2% (12 months to May increased by 4%)

Bacs Direct Debit values have increased by 7% (12 months to May increased by 8%)

Total Bacs values have increased by 3% (12 months to May increased by 5%)

Volumes for Bacs Direct Credits in June 2022 decreased by 3% when compared with June 2021. This is possibly timing given the month on month increase of 14% in May 2022 compared to May 2021 with the later bank holidays bringing forward payments into May. With similar conditions now in place ongoing volumes are likely to be more closely in line across the two years.

Growth in Direct Debit volumes year on year is still seen, now at 3% for the 12 months to June 2022 when compared with the 12 months to June 2021. As Direct Debits account for 70% of Bacs payment volumes, this has helped to maintain the overall growth seen over the year although there is a slight reduction to 2% when compared with the year ending June 2021.

Year on year growth for the value of Bacs Direct Credits has fallen back slightly to 2% for the 12 months ending June 2022 with the value of Bacs Direct Credits processed in the month itself decreasing by 7% for June 2022 when compared with June 2021.

Growth in the value of Direct Debits is also seen although at a lower rate with the value processed in June 2022 being just 5% greater than in June 2021.

CHAPS

In the 12 months to the end of June 2022 we see that:

CHAPS volumes have increased by 7% (12 months to May increased by 10%)

This was made up of a 7% increase in retail / commercial based payments and a 6% increase in financial institution payments, compared to 11% increase and 5% increase respectively for the 12 months to May.

CHAPS values have increased by 2% (12 months to May increased by 1%)

This month the change was made up of an 2% increase in retail / commercial based payments and a 2% increase in financial institution based payments, compared to 1% increase for both for the 12 months to May.

Retail / Commercial payment activity had fallen throughout 2020 recovering in December before falling back again in January 2021. Volumes have since recovered although for June they decreased by 7% when compared with June 2021. Values also recovered although the increase in June 2022 is just 6% when compared with June 2021.

The underlying resilience in Wholesale payment volumes has continued although volumes in June 2022 increasing by just 3% when compared with June 2021. Wholesale CHAPS values for June 2022 compared with June 2021 have also increased but again by just 2%. Overall this has continued to lead to a year on year increase In values with Wholesale payment values increasing by 2% for the year to June 2022 compared to the year to June 2021 – in May the Increase had been 1%.

Faster Payments

In the 12 months to the end of June 2022 we see that:

Single Immediate Payment volumes have increased by 18% (12 months to May 20%)

Total Faster Payment volumes have increased by 17% (12 months to May 19%)

Single Immediate Payment values have increased by 22% (12 months to May 24%)

Total Faster Payment values have increased by 21% (12 months to May 24%)

The trend has continued in June with both volumes and values ahead of 2021 levels. June 2022 saw an increase of 6% in the volume of Single Immediate Payments processed in the month compared to 2021 and 15% in the value of Single Immediate Payments.

The widespread use of faster payments is a digital payment habit that will be here to stay, reinforced throughout each lockdown and with volumes and values continuing to increase month on month. Although the trajectory has flattened a little particularly when similar conditions have been in place, an overall significant increase year on year looks set to continue for some while to come – particularly with inflationary pressures also having an impact on the value of payments processed.

Keep reading with a 7-day free trial

Subscribe to Payments:Unpacked to keep reading this post and get 7 days of free access to the full post archives.