27 days until R-Day

Issue 647: 10 September 2024

Did you know that it’s only 27 days until Monday 7 October 2024: R-Day!

What’s R-Day?

R-Day is the day that mandatory APP fraud1 reimbursement requirements come into force in the UK.

A revision, scope extension, a clarification and some data

With under a month to go here’s four last minute APP “nuggets”you should know:

A revision

When the PSR published its requirements for payment firms to reimburse APP scams victims in December 2023 they committed to consider high value APP fraud claims and publish the findings.

When the PSR published their requirements for payment firms to reimburse APP scams victims in December 2023, they committed to consider high value APP fraud claims and publish the findings.

The PSR has published its review, which found that – out of over 250,000 cases - there were 18 instances in 2023 of people being scammed for more than £415,000, and 411 instances of more than £85,000.

The analysis also highlighted that almost all high value scams are made up of multiple smaller transactions, reducing the effectiveness of transaction limits as a tool to manage exposure.

The PSR have stated that they have considered additional evidence from the industry and FCA (and MHT) about the maximum liability amount.

After considering the findings and evidence provided, the PSR are consulting on a new cap. If confirmed, this would bring the cap in line with the Financial Services Compensation Scheme (FSCS) limit which is currently £85,000 and well understood by consumers.

This would still ensure enhanced consumer protections against APP scams, with clear incentives on financial firms to continue doing all they can from preventing fraud from happening in the first instance.

The previous maximum reimbursement value had been set at £415,000, in line with the Financial Ombudsman maximum reimbursement limit at that time.

The proposed new cap will still see over 99% of claims (by volume) covered. The PSR have also committed to keeping this under consideration through via the post-implementation review.

The PSR fully expects all firms to meet their obligations as responsible providers and will continue to follow up with all firms to support this.

The consultation closes on 18 September and the PSR will consider the responses carefully and confirm their final approach before the end of September.

The PSR have also confirmed that their requirements will still come into effect from 7 October 2024.

Scope extension

The PSR have published a policy statement and Specific Direction 21, expanding APP scam reimbursement protections to consumers of CHAPS.

In May, the PSR consulted on the proposal to direct banks and other payment firms participating in CHAPS to reimburse their customers who have been victims of authorised push payment (APP) scams. The proposed direction is designed to underpin the Bank of England’s new CHAPS reimbursement rules.

The PSR have confirmed the approach that they are taking to expand reimbursement protections to consumers of CHAPS. The proposed rules, the approach which they consulted on and SD21 are aligned with the approach they are taking for Faster Payments.

This policy statement sets out the final details of the CHAPS reimbursement requirement policy, and confirms:

the policy start date of 7 October 2024, aligned with the date that the Bank’s CHAPS reimbursement rules will come into effect, and the Faster Payments reimbursement policy start date. This approach will ensure delivery of consistent protections for consumers of CHAPS to be delivered as soon as possible, and reduce the risk of fraud migrating from Faster Payments to CHAPS.

all in-scope PSPs must register in line with the requirements set out in the CHAPS reimbursement rules as soon as practicable and no later than 7 October 2024, by providing the information set out in the CHAPS reimbursement rules. This requirement only applies to PSPs who are not already required to register (or who are not already registered) with Pay.UK as required by SD20 which applies to directed PSPs in relation to Faster Payments. This is to ensure that in-scope PSPs are only required to register once.

the compliance and monitoring metrics PSPs will need to report to the Bank on a monthly basis. This information may also be shared with the PSR so that they can monitor compliance with SD21. These are aligned with the confirmed metrics for Faster Payments – with a key difference that PSPs are not required to submit nil returns to the Bank, where they have not received any APP scam claims in the relevant reporting period.

A clarification

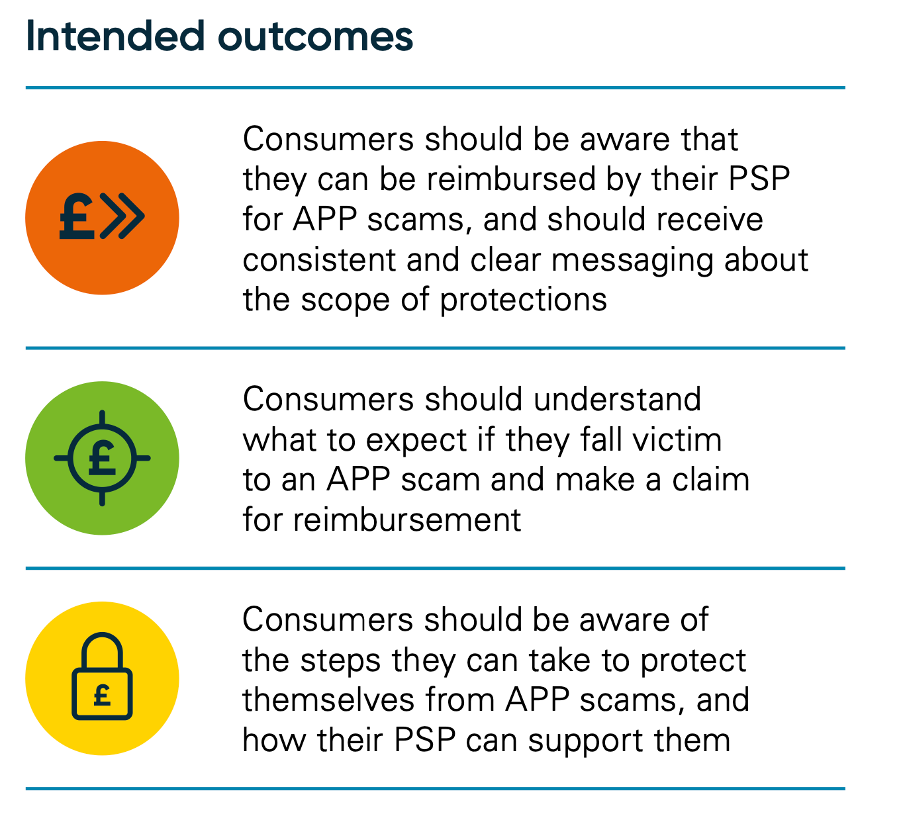

In the PSR’s Specific Direction 20 (SD20), they require sending payment service providers (PSPs) to inform existing consumers of their rights under the reimbursement requirement and rules.

The PSR has published information on consumer communications for PSPs, aiming to facilitate compliance with our SD20.

The purpose of the document is to facilitate compliance with PSR’s SD20 (July 2024). The PSR are not prescribing how firms should communicate to their consumers and PSPs should have the flexibility to communicate with their consumers in ways which reflect their business model and approach.

Source: PSR

This document does not preclude any additional communications PSPs may wish to provide to their customers in respect of the requirements. PSPs should continue to have regard to FCA Consumer Duty requirements and any other relevant regulatory obligations.

Specific Direction: Requiring sending payment service providers (PSPs) to inform existing consumers of their rights under the reimbursement requirement and rules:

Additional information on consumer communications for PSPs, aiming to facilitate compliance with the PSR’s SD20:

Some data (How well is your bank doing?)

Keep reading with a 7-day free trial

Subscribe to Payments:Unpacked to keep reading this post and get 7 days of free access to the full post archives.