Regulate, Consolidate, Reduce

A £26 million budget, a 7% efficiency saving and a phased merger with the FCA — here's what the UK's payments regulator has planned for its penultimate year of independent operation

Regulate, Consolidate, Reduce

The other day someone asked whether I enjoyed my time as a Senior Adviser at the Payment Systems Regulator (PSR) - the world’s first (and last?) dedicated systemic payment system regulator (my answer BTW was ‘yes’).

This led to a discussion about what the PSR was up to as it went through the process of being consolidated into the Financial Conduct Authority (FCA). As we discussed the PSR’s planned activity for 2026/27 it occurred to me that six weeks ago the regulator published their annual plan and budget and I hadn’t covered it in Payments:Unpacked.

So to rectify that omission here’s a quick summary of the PSR’s plan for 2026/27 - possibly the last stand alone plan we’ll see ahead of consolidation into the FCA.

Foreword from the top

In his foreword David Geale (the PSR’s Managing Director) paints his view on the state of play - here’s a summary of David’s message:

The UK’s Payment Systems Regulator enters 2026/27 with genuine momentum. Over the past year it has delivered world-leading APP fraud protections, progressed action on card fees, and shaped the next generation of retail payments infrastructure. Its 2026/27 programme builds on this — tackling cross-border interchange fees, implementing scheme and processing fee remedies, overseeing critical infrastructure delivery, and supporting the FCA on open banking. All of it delivered with a budget 7% lower than last year and a 20% reduction in the annual funding requirement for fee payers.

The bigger story is what comes next.

The PSR is consolidating into the FCA, with legislation proposed to transfer all powers and functions across. Staff are already operating under the FCA’s structure in a phased transition, while the PSR continues as an independent regulator with its own board. The message from Chair David Geale is clear: the economic regulation of payment systems is as important as ever — the vehicle delivering it is simply changing.

Statutory Objectives

As you would expect the PSR’s work seeks to support the regulators statutory objectives to promote:

competition

innovation

the interests of the people and businesses that use payment systems.

Work Programme

The PSR’s work programme for the year ahead seeks to embed many of the changes that the PSR set out last year. The PSR state that they will “maintain momentum on major, long- term initiatives while responding to new challenges”.

Not surprisingly the plan comprises of a smaller number of initiatives that we have come to expect in a PSR’s annual plan - there are eight key elements to the plan:

1: Delivering the National Payments Vision (NPV)

We will continue to work closely with the Bank of England, the FCA and the Treasury as part of our role on the Payments Vision Delivery Committee (PVDC). Specifically, we will support the design and build of the future infrastructure, recognising the anticipated regulatory roles of the PSR and the FCA alongside the Bank of England, and furthering our statutory objective on innovation. We will also continue to oversee Pay.UK and the short-term enhancements to Faster Payments.

PSR 2026/27 Annual Plan and Budget

2: Continuing action on APP Fraud

Our work fighting APP fraud is having a big impact: payment firms reimbursed £173million to victims in the first year of our reimbursement requirement. These world-leading measures build trust among consumers and give firms an incentive to prevent fraud, strongly supporting our statutory objective to promote the interests of the people and businesses that use payment systems.

This year, we will publish the independent evaluation of the first year and consider if we need to take further action. We will also continue to collect and monitor data to show the impact of our work transparently and clearly. If firms do not meet the standards we expect, we will engage with them and decide what action to take.

PSR 2026/27 Annual Plan and Budget

3: Enhancing approach to supervision and enforcement

We will continue to refine our supervision and enforcement models, building on our existing capabilities. We will also align our supervisory model with FCA practices. This will enhance our oversight of the firms we supervise, so that this will continue in the most effective way after our consolidation with the FCA, in support of all of our statutory objectives.

PSR 2026/27 Annual Plan and Budget

4: Take Action on card fees

Cards are the most popular retail payment method. However, the lack of alternatives for merchants affects competition and innovation, with knock-on impacts for the people and businesses making payments.

Cross-border interchange fees have increased more than five- fold since the UK left the EU, by £150–200 million a year. Last year, we consulted on remedies but paused further action in light of ongoing litigation. Since then, the High Court has confirmed our powers to price regulate. We continue to progress our work and consider next steps.

Domestic scheme and processing fees increased by over £170 million a year in real terms between 2017 and 2023.

In March 2025, we consulted on remedies to address a lack

of competition in the market. In December we issued draft directions on pricing governance, and information, transparency and complexity. This year we will consult on our final remedy on regulatory financial reporting, and monitor compliance with our requirements.We will provide our expert regulatory insight in the Merchant Interchange Fee Umbrella Proceedings before the Competition Appeal Tribunal.

PSR 2026/27 Annual Plan and Budget

5: Develop a cards market strategy

We will consider our approach to competition in cards markets in the round, taking account of other market developments. This will help determine how best we can meet our competition objective, and support the FCA in determining the best way to regulate these markets going forward.

PSR 2026/27 Annual Plan and Budget

6: Driving Forward Open Banking

Open banking in the UK is growing rapidly and has the potential to offer a competitive alternative to cards in UK retail payments and support payment services innovation. The latest industry figures show that more than 16 million users now benefit from the service. The number of open banking payments has soared by 53% year-on-year, reflecting a significant shift in how consumers and businesses manage their finances. We will continue to support the FCA in establishing a long- term regulatory regime and a future entity to oversee open banking. This work builds on last year’s formation of the UK Payments Initiative (UKPI) and the phase one roll-out of variable recurring payments (VRPs).

PSR 2026/27 Annual Plan and Budget

7: Evaluation of the card acquiring market review

We will review the effectiveness of the specific directions we issued following our market review into the supply of card-acquiring services, which aimed to further our competition objective.

PSR 2026/27 Annual Plan and Budget

8: Support consolidation with the FCA

Consolidation will be a critical priority for the coming year, with robust planning and coordination helping us manage its impact across the organisation and on our stakeholders. We aim to ensure a smooth and orderly transition, while continuing to deliver our priorities and preserving the independence of the PSR until we are legally consolidated. Across our work, we will provide clarity and certainty for regulated entities so they can continue to focus on their core activities.

PSR 2026/27 Annual Plan and Budget

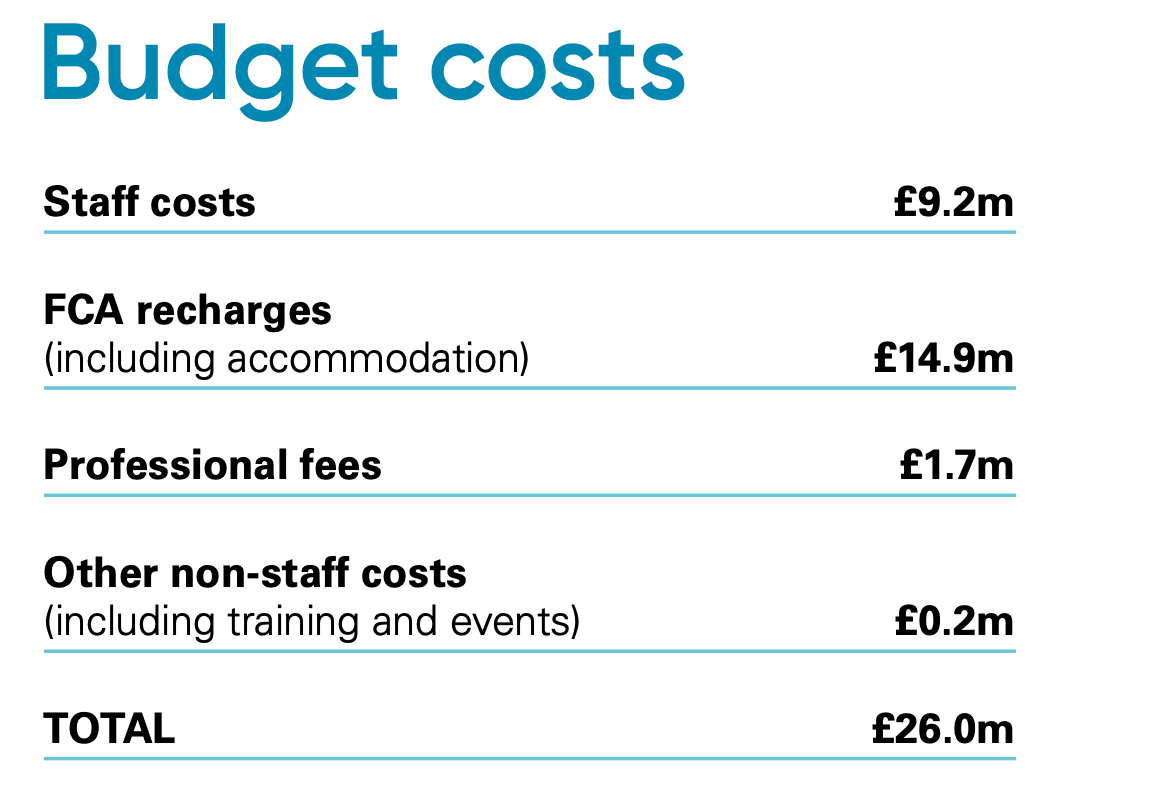

2026/27 Budget

The PSR’s 2026/27 budget is set at £26.0 million — 7% lower than the previous year. Around £14.9 million covers FCA Shared Services costs as more internal functions transfer across, with the regulator leaning increasingly on the FCA’s operational infrastructure to deliver its work cost-effectively.

Of the total budget, £21.5 million will be recovered from fee payers through the annual funding requirement. The remaining £4.5 million will be drawn from accumulated reserves, leaving approximately £1.5 million in reserve at year end. The PSR is deliberately absorbing transition costs itself rather than passing them to fee payers, with any additional consolidation costs expected to be contained within the existing budget envelope.

Regulate, Consolidate, Reduce

A £26 million budget, a 7% efficiency saving and a phased merger with the FCA — here’s what the UK’s payments regulator has planned for its penultimate year of independent operation

Download the full plan and budget here: