Kein SWIFT for Russland?

Kein SWIFT for Russland?

Issue 275 | 26 February 2022

Kein SWIFT fur Russland?

From gas pipes across Europe to financial messaging systems the invasion of Ukraine has brought access to and the operation of global infrastructures during a time of crisis into question.

European Union foreign ministers have discussed banning Russia from the SWIFT financial messaging network, which is pivotal for the smooth operation of payment systems worldwide.

A complex decision

Although Russia accounts for just 1.5pc of SWIFT activity deciding what to do is complex.

The BBC described the challenge as:

Banning Russia from the system - used by thousands of financial institutions - would hit the country's banking network and access to funds. There would, however, be blowback on other countries and companies because, for example, buying oil and gas from Russia would be disrupted.

Ben Wallace, the UK’s Defence Secretary stated:

Britain wants the SWIFT system to be turned off for Russia. But unfortunately the SWIFT system is not in our control. It is not a unilateral decision.

But Germany's foreign minister, Annalena Baerbock stated that Berlin did not believe excluding Moscow from the Swift was the right thing to do at this moment stating:

I can understand - I feel the same way - that in these minutes, in these hours, emotions are running high and that words like 'SWIFT Agreement' sound very, very strong, but at these moments you have to... keep a cool head.

The challenge is not without precedent as in 2012 SWIFT ejected Iranian banks with from the SWIFT network. The possibility of restricting SWIFT access from Russia is, therefore, possible but complicated.

SWIFTs positions described here: SWIFT and sanctions - in this document SWIFT states:

SWIFT is neutral. The Company is set up and operated for the collective benefit of its Shareholders, for the study, creation, utilisation and operation of the means necessary for the telecommunication, transmission and routing of private, confidential and proprietary financial messages.

SWIFT is a messaging service provider and has no involvement in or control over the underlying financial transactions:

SWIFT complies fully with all applicable sanctions laws. Responsibility for ensuring that individual financial transactions comply with sanctions laws, however, rests with the financial institutions handling them, and their competent authorities. SWIFT is only a messaging service provider and has no involvement in or control over the underlying financial transactions that are mentioned by its financial institutional customers in their messages.

A decision might be down to Belgian law and EU sanctions:

In March 2012, pursuant to international and multilateral action to intensify financial sanctions against Iran, EU Regulation 267/2012 was passed. The Regulation prohibits specialised financial messaging providers, such as SWIFT, from providing services to EU-sanctioned Iranian banks. SWIFT is incorporated under Belgian law and has to comply with this decision as confirmed by its home country government. SWIFT implemented the regulatory obligation by disconnecting the related EU-sanctioned banks.

Way above my pay grade

Commenting on the invasion of Ukraine and the use of sanctions in a (the only) global financial messaging system is way above my pay grade.

However, with payments and SWIFT featuring in mainstream media over the past few days it’s a good time to share a SWIFT 101 - especially as Chris Higham has reminded us that SWIFT is not actually a payments system.

SWIFT changed the world (and helped me get a promotion)

Almost 50 years ago SWIFT changed the way that banks around the globe communicated and enabled financial transactions to change forever.

SWIFT replaced TELEX based Telegraphic Transfers (TT’s) - Go Cardless describe TT’s as:

The term “telegraphic transfer” has its origins in the way that banks used to make international money transfers. Essentially, transfers would be made with the ‘Telex’ network of teleprinters – electronic machines that communicated via text-based messages that were used to arrange transfers.

My first experiences of payments in correspondent banking were at the very end of the TELEX (one of my jobs was to interpret a free format TELEX message with a red pen and a ruler to ‘mark up’ the message into a payment instruction that a typist could enter into the ‘system’ ready for a first, second checker and a ‘releaser’ to send the payment to the beneficiary. Hardly STP (Straight Through Processing)!

In my interview to become a ‘funder’ I was asked what SWIFT stood for - getting the ‘I’ right got me the job. I was then introduced to the world of MT101’s, MT210’s MT940/950’s, SHA / BEN / COR charging options and, worst of all, a free format MT999.

From humble correspondent banking to treasury deals it is fair to say that SWIFT has transformed global financial trade but as we know:

With Great Power Comes Great Responsibility.

Uncle Ben, Spiderman, 2002

SWIFT: Society for Worldwide Interbank Financial Telecommunication

Noting that the invasion of Ukraine and the use of sanctions in a (the only) global financial messaging system is way above my pay grade let’s spend the rest of our time unpacking what SWIFT actually is.

We are grateful to Santosh Rajagopalan at Payments Domain as he helps us unpack the financial messaging system known as SWIFT…….

The year was 1973, the world was changing rapidly. The United Kingdom, Denmark, and Ireland entered the European Economic Community, The first American prisoners of war were released from Vietnam, The Exorcist premiered for the first time and the world of payments changed forever and for the better. Banks back then had a big problem when trying to make international payments “Communication!!”

Banks used a technology called TELEX (Telegraphic Exchange) which was a major method of transmitting written messages between businesses. It was basically a network of teleprinters that used telegraph-based connections. Think of TELEX like a texting service that we use today so commonly but using large machines. This was even before FAX became popular. TELEX was basically the latest version of the telegram that has been in use since the 19th century.

TELEX had several downsides. It was slow, there was no security and the worst part was that the receiver was not able to understand the instruction (aka payment messages). A lot of details got lost in translation. There was no universal standard for communication between banks. There were language barriers, time zone differences, human errors which all led to one thing – Change.

This change came in the form of a co-operative that decided to formulate and structure how financial information was shared between banks which would result in a revolution in the cross-border payments space that stood the test of time. In 1973, 239 banks from 15 countries joined hands to bring an end to this communication conundrum by forming SWIFT.

SWIFT stands for Society for Worldwide Interbank Financial Telecommunication and contrary to popular belief it is not a government body but a co-operative of banks. The headquarters was established in Belgium. In the next 4 years a messaging standard, a platform for exchanging these messages, and a powerful computer to route the messages were all put in place and the new system went live in 1977. This service that was offered by SWIFT was unlike anything that existed before. It was a game-changer in the financial world.

By the time it went live, the word was out and 518 intuitions from 22 countries were part of this network. Confidentiality, efficiency, security, and reliability were the main agenda so much so that 12 million transactions were processed during the first year in this new age wonder.

In the early 80s, the ‘SWIFT COMMUNITY’ expanded and the number of banks grew more than 1000 from 52 countries. The east, especially the APAC region joined the party.

The 1990’s pushed the technological boundaries; the availability rate of the SWIFT network was close to 100 %. SWIFT as a community kept growing and stayed relevant throughout the years as it understood the market well, supported the community well, and was open to changes whenever necessary.

Today there are 11,000+ institutions that SWIFT connects and aids in the exchange of more than 8.4 billion messages. Truly a remarkable feat.

At the timing of writing this article, SWIFT is gearing up for one of the largest changes in the history of financial messages. SWIFT has decided to let go of its proprietary messaging standards the “MT messages” and is now going to move to “MX messages” which is based on ISO20022. Standardisations are always difficult to execute that to envision. There should be a legitimate business reason for such a transition which we will explore further.

SWIFT MTs from a Payments Perspective

SWIFT MT messages have been the backbone of international finance for years now. Yes, you read it right. Finance, which included payments, Trade Finance, Treasury, FX, Securities, etc.

There are different categories of MT messages for each of the categories mentioned above.

There is a total of 9 + 1 categories:

Out of all these categories of message we are going to focus on three main categories of MT messages

Category 1 – MT1 series

Category 2 – MT2 series

Category 3 – MT9 series

Category 1 aka. MT1 Series:

This series of messages are used for customer ( of banks) initiated payments and checks. Messages from this category are used to initiate and transfer customer-related payments. Some examples of such messages are

MT101 – Used by bank’s customers to initiate a payment

MT103 – Used by banks to sends funds to each other

MT104 – Used for Direct Debit payments

MT191 – Used for sending charge requests to other banks

We will of course see in detail about the individual messages but just give you a better idea on this category let us take an example to understand the usage of these messages.

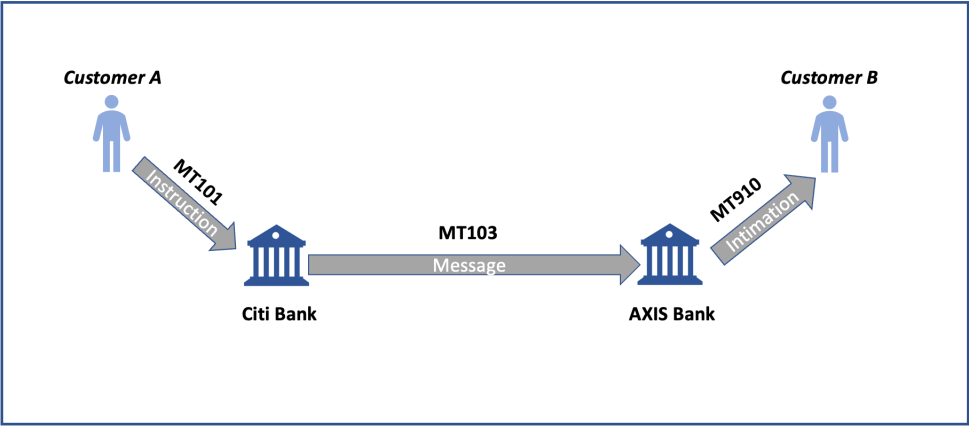

Customer A (Of Citibank) Initiates a payment to Customer B (of AXIS Bank) and this is done using the MT101.

Now, Citi Bank sends the funds to Axis bank using the MT103. The reason for using a 1 series message is that this transaction involves an underlying customer of the bank.

Once Axis banks credits the funds to customer B it intimates by sending an MT910. MT910s are not a part of the category 1 messages but still it is worth mentioning the same at this point.

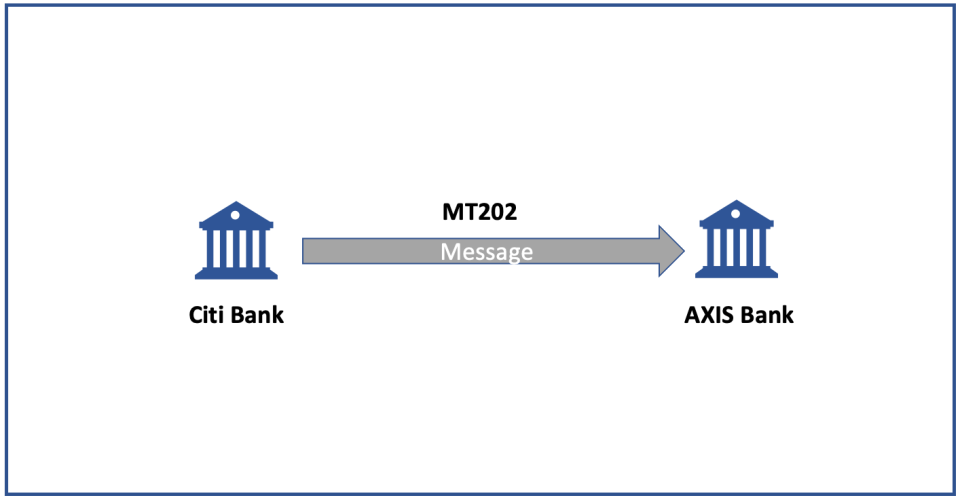

Category 2 aka. MT2 Series:

These messages are used by banks to send funds to each other. You might very well ask “What is the difference between a category 1 and 2 as both are used by banks to send funds to each other??!!”

Here is the difference, If a category 2 message is used then there should be no customers involved and all the parties in the chain must be financial institutions.

An example of such a transaction would be Citibank sending fees to AXIS bank. Another example is to move funds between two of its accounts.

Category 9 aka. MT9 Series:

These messages do not carry funds but are used to send details of the cash position of different parties to others. We have already seen an example in the category 1 message above.

These messages are used for the following purposes:

Confirmation of debit of an account

Conformation of credit to an account

Account statements

Interim status reports

103, 202 and 104: What do they mean?

Another question you might have regarding the numbers 103, 202 .. What do they mean? Is there a logic behind the names?

SWIFT MT messages have a very simple naming convention, it is easy to understand and is straightforward.

The first question that might pop up in our mind is, “what does MT stand for??” MT simply stands for Message type.

This is followed by a 3-digit number

1st Digit – Category of the message. Describes the underlying business function of the message. Example: Category 1 = Customer Payments and Cheques.

2nd Digit – Group of the message. Describes the function of the message within the specified category. Example: 11n = Category 1 Cheque Payment Messages.

3rd Digit – Type of the message. Describes the specific function. Example: 112 = Status of a Request for Stop Payment of a Cheque.

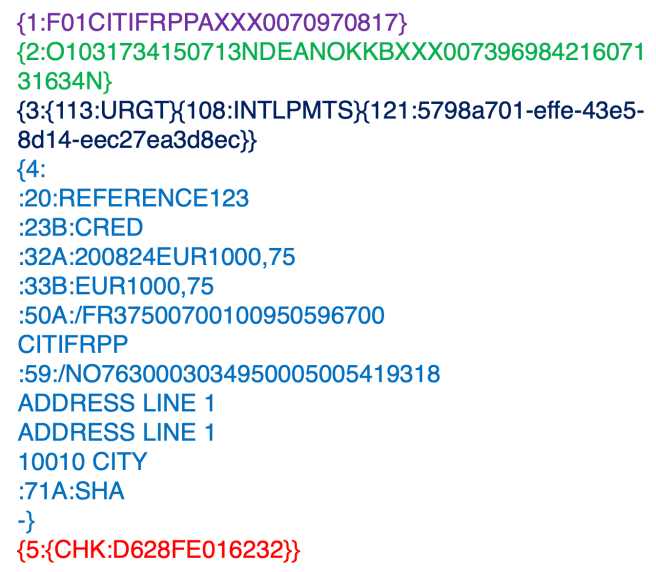

Let us now take an example of a simple MT103 and try to understand the name

SWIFT message blocks

There are a total of 5 blocks in a SWIFT message. Each block starts with the block number and contains a specific set of data.

The original message type that was developed by SWIFT and a subset was later made into ISO15022.

Thank you Santosh

Thank you to Santosh for this SWIFT Masterclass - perhaps calling this blog a SWIFT 101 would be a bit confusing:

MT 101 SWIFT message is a payment request sent to the bank that will perform the payment transaction by the sender's bank through SWIFT, and may include one or multiple payments orders to be made from the accounts at the bank that will perform the payment transaction.

About Santosh

Santosh Rajagopalan has been a part of the software industry since 2012. He has worked with a number of organisations including Accenture, Capgemini, Société Générale, and Temenos working primarily on large-scale payments transformation projects for banks across three continents. Santosh is currently working as a payments business analyst but has a strong interest in quality assurance.

Santosh writes:

This article is my way of saying goodbye to MT messages plus I think it is critical to know MT messages well for us to understand the MT to MX transformation. Santosh Rajagopalan, Payments Domain.

Help grow Payments:Unpacked’s audience

If you enjoy reading Payments:Unpacked please share with your friends and colleagues.

Or subscribe: