Keep on Running

In our third Faster Payments newsletter from Jeremy Light’s Agenda:Payments newsletter we explore what’s next for Faster Payments in the UK - huge thanks to Jeremy for allowing Payments:Unpacked to feature this guest blog.

Be sure to subscribe to Jeremy’s excellent Agenda: Payments newsletter at:

The UK’s Faster Payments system (FPS) has had a profound impact on consumer and business payments. As the only system of its kind when it launched in 2008, it led the way in real-time payment adoption which has become ubiquitous globally.

The UK may rank only 22 in the 2024 real-time payments per capita index I compiled with 69 countries last year1 but it understates the effect FPS has had in influencing the decisions, design, implementations and operation of the 40+ real-time interbank payment systems running today.

What is this impact in the UK and the world, what have we learnt from FPS and what comes next?

UK Impact

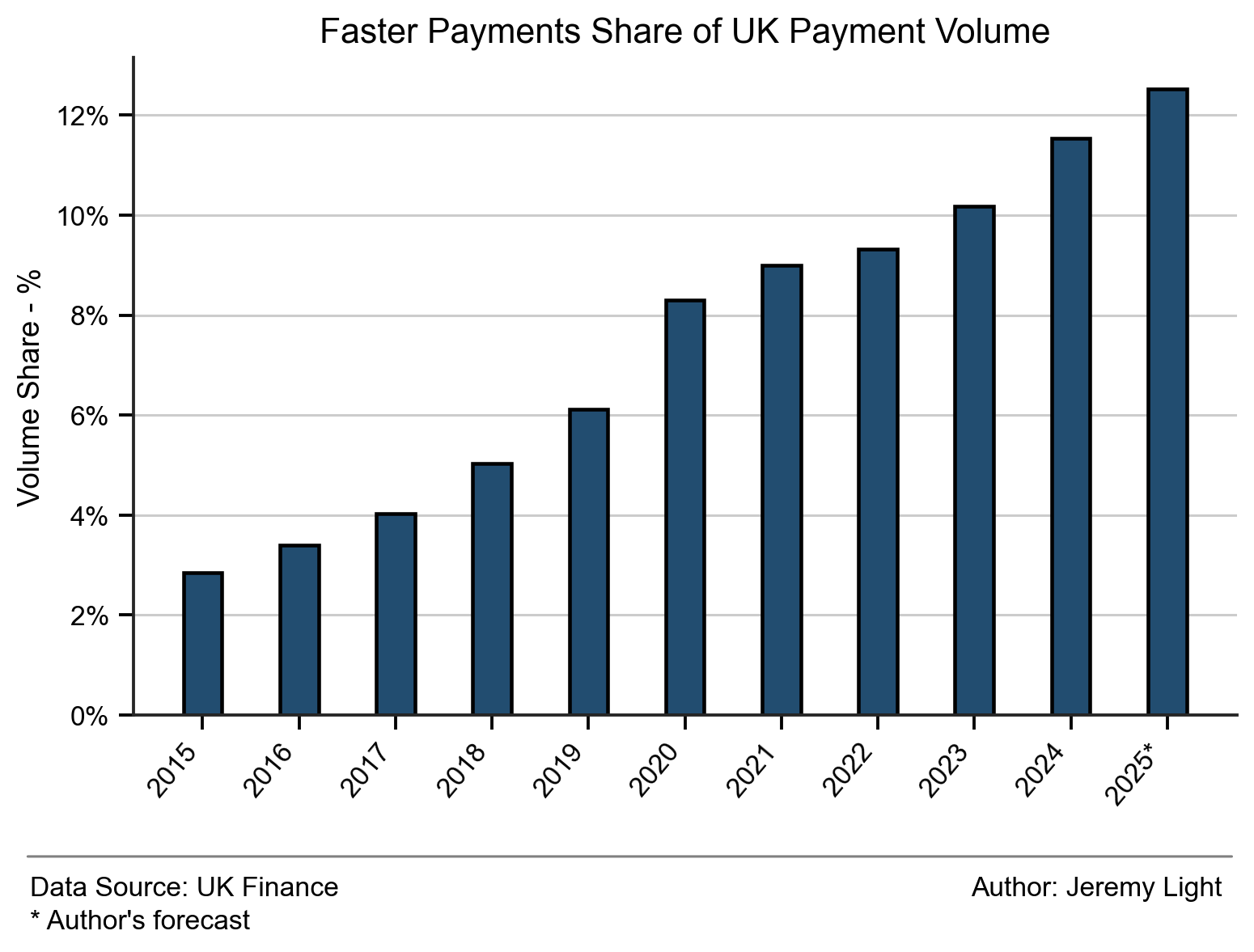

FPS processes more than 12% of all payments in the UK by volume of transactions (including cash), up from around 3% 10 years ago, as shown in Figure 1. Over the same period, UK payment volume has grown 34% - driven in large part by contactless debit cards but also by FPS. Faster Payments growth has been due to much more than just substitution of cheque and bill payments through Bacs.

Cheque volumes are down 470m payments in annual volume since 2016 and Bacs direct credits are down 276m payments2. Meanwhile, Faster Payments are up 5bn payments over the period. It has created its own payment domain that is fuelled by the atomisation of payments – paying more often in smaller amounts3.

Figure 1 – Faster Payments volume share of UK payments (including on-us payments)

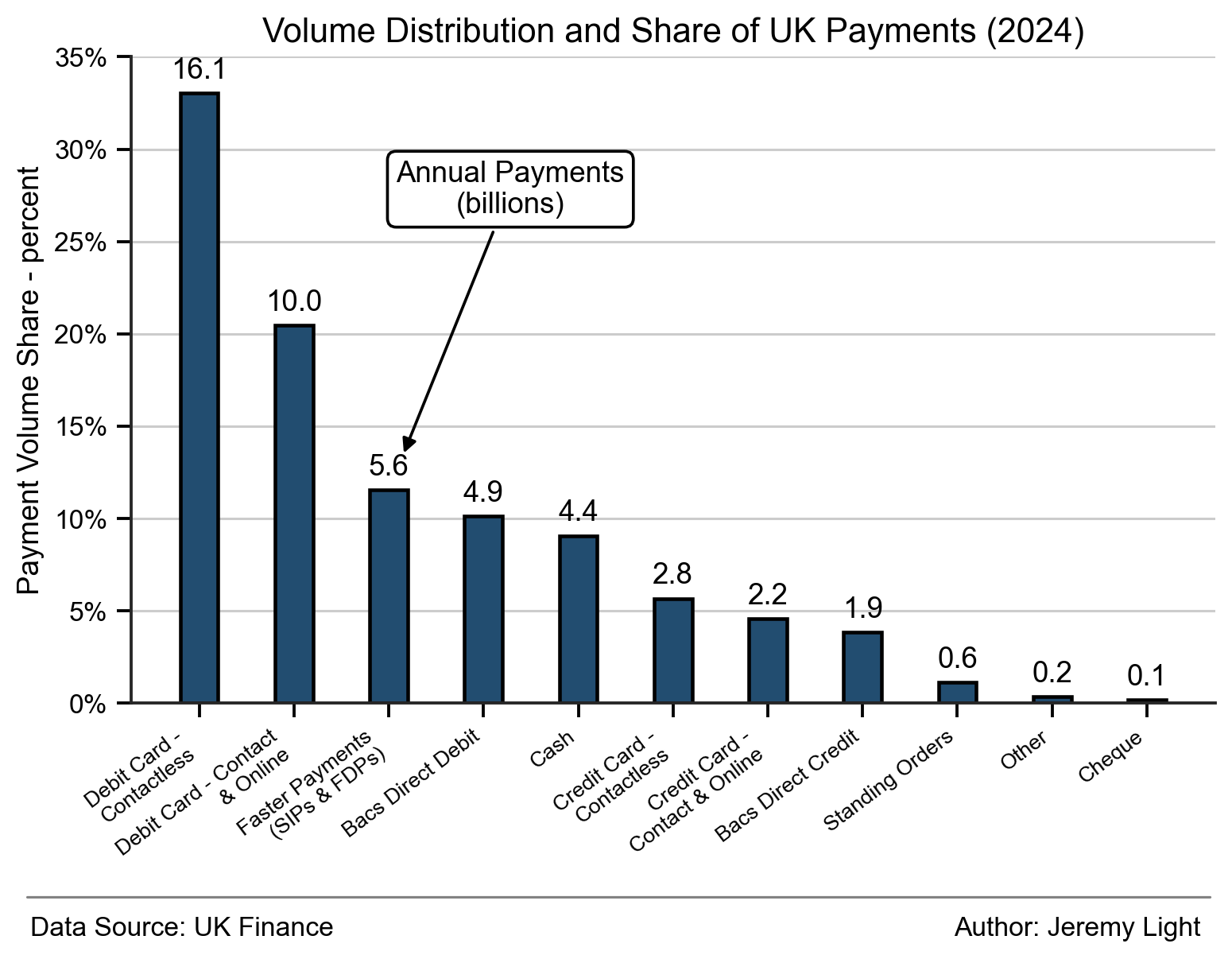

After contactless debit card and non-contactless debit card payments, FPS is the third largest source of payments by volume in the UK. See Figure 2.

Figure 2 – Volume share of UK payments (excluding CHAPS – 0.1%; including on-us online banking payments in the Faster Payments figure)

FPS also has had a major impact on the success of the Fintech challengers, such as Clearbank, Monzo, Revolut, Wise and Starling. Clearbank launched in 2017 as a direct participant of FPS and as an access provider for indirect participants, enabling it from the start to differentiate itself from the established sponsor banks with a real-time 24/7 offering to agency banks and PSPs. Monzo, Revolut, Wise and Starling launched to provide a better, modern, digital-first customer experience for cross-border payments and bank accounts. Making this experience real-time with real-time payments and balance updates was critical to their propositions.

Global Impact

Today, there are around 40 – 50 countries with real-time interbank clearing and settlement systems and they keep coming on stream – the most recent is the METIX/SPIM system in Mozambique launched last month (3rd March)4. The experience of the FPS and insights from it have had a major influence on many of these systems around the world.

For some, the influence has been direct, where Vocalink has provided technology support, including software it developed for export (before being acquired by Mastercard). Vocalink software powers PromptPay in Thailand, FAST in Singapore and RTP at The Clearing House in the USA (and possibly others). This software has proved itself, with Thailand number three in the global real-time payments per capita index I compiled last year (footnote 1) and Singapore at number four.

Lessons from Faster Payments

The past 18 years of Faster Payments operation have provided many lessons for the payments industry.

Perhaps the most important is that the value proposition for real-time payments is certainty with immediacy, rather than just immediacy. Immediacy is obviously essential for situations such as when selling goods and services but less so when paying, for example an electricity bill.

However, immediate certainty that a payment is received and final is a critical feature for all real-time payments – an immediate confirmation means no waiting, no checking a payment has gone through, no reconciliation (of payments received to payments expected), no chasing, no estimating (of cashflows and balances), no tracing, no investigation, no missing payments. The impact of immediate payment certainty on the user experience and on business capabilities is profound.

Other lessons include:

1. Reliability of the core engine is critical – FPS has run continuously for 18 years with just one short hiccup. Its fault tolerant, nonstop architecture has been a bedrock underpinning its success.

2. Versatility drives adoption – FPS is versatile through supporting synchronous (real-time) and asynchronous payments (standing orders, forward dated, corporate direct) with one connection, which facilitated the transition from legacy in the early days and makes the system attractive for multiple uses by multiple participants today.

3. Indirect participation in a real-time payment system needs to have real-time, 24/7 connectivity and processes, otherwise the benefits of real-time payments are lost. The traditional batch model of indirect participation is unsuitable.

4. Settlement accounts held at the central bank by non-banks help level the playing field for new entrants and non-banks, as evidenced by the demand for them in the UK. Real-time payments require active intraday liquidity management (prefunding in the UK) and settlement accounts improve liquidity control and efficiency for participants.

5. Open access to the core engine promotes competition and levels the playing field. FPS’s New Access Model allows direct connectivity to the central infrastructure through technical aggregators and has been a big success, creating a competitive market and strong network effects that have driven volume.

6. Real-time payments allow supply chains to be reinvented – just-in-time payments that are real-time, speed up supply chains and improve efficiency e.g. by enabling just-in-time ordering that reduces/eliminates inventory.

7. Real-time payments have exposed weaknesses in financial crime controls. Authorised push payments fraud (APP) has become a problem as FPS usage has increased. Real-time payments mean fraudulent payments can be received and forwarded instantly, well before victims realise they have been scammed and before banks can investigate. This is an account management problem rather than a payments problem and it has meant that banks have needed to strengthen their controls to prevent the opening of fraudulent accounts and to identify compromised accounts. APP fraud in the UK is under control but it is still significant.

8. Regulators need to act quickly to innovation, as well as be open-minded - for example, non-bank settlement accounts are segregated, single purpose, prefunded, relatively low balance accounts and pose little risk to financial stability (and are different to reserve accounts). The Bank of England deserves credit for being open-minded in pioneering non-bank settlement accounts and has led in the world in implementing them. Yet it still took over four years to agree and implement them on its RTGS, delaying the significant impact these accounts have made in the UK, despite their low risk and large benefits.

A final lesson to highlight is that real-time payments systems like FPS can be a foundation for innovation and overlay services. This is seen more in other countries such as India, with UPI. UPI is an overlay service on the IMPS real-time payment system which is similar to FPS. Built on a fault-tolerant, nonstop system based on card/ATM technology, IMPS processes about 1.4% of electronic payments in India, compared to FPS’s 13% (excluding cash) in the UK. However, IMPS enables the UPI overlay service which processes 86% of electronic payments in India, 20bn per month. FPS has overlay services like confirmation of payee but unfortunately it lacks one for consumer payments like UPI in India or PayNow in Singapore.

In my opinion, this has been a missed opportunity for FPS so far, which is why despite being a pioneer and a stalwart in real-time payments, other countries such as India and Singapore have forged ahead.

FPS Future

FPS has been in operation for 18 years and is likely to continue for many more. There have been plans to upgrade or replace it going back to 2015, including the New Payments Architecture, a grand projet which has been discontinued – FPS has survived them all.

Now, UK regulators have come up with a different approach, the Interbank Infrastructure Renewal programme under the National Payments Vision, with a focus on resilience and innovation.

FPS, with its fault-tolerant, nonstop architecture ticks the resilience box in spades. There are incremental improvements needed, such as certainty of fate rules (recently clarified5) to help with open banking payments at POS and for ecommerce; potential liquidity improvements when the Bank of England starts extending RTGS opening hours6; and perhaps a move to implement the (often misunderstood) ISO20022 data standard.

However, it is on the innovation side where FPS has the most potential.

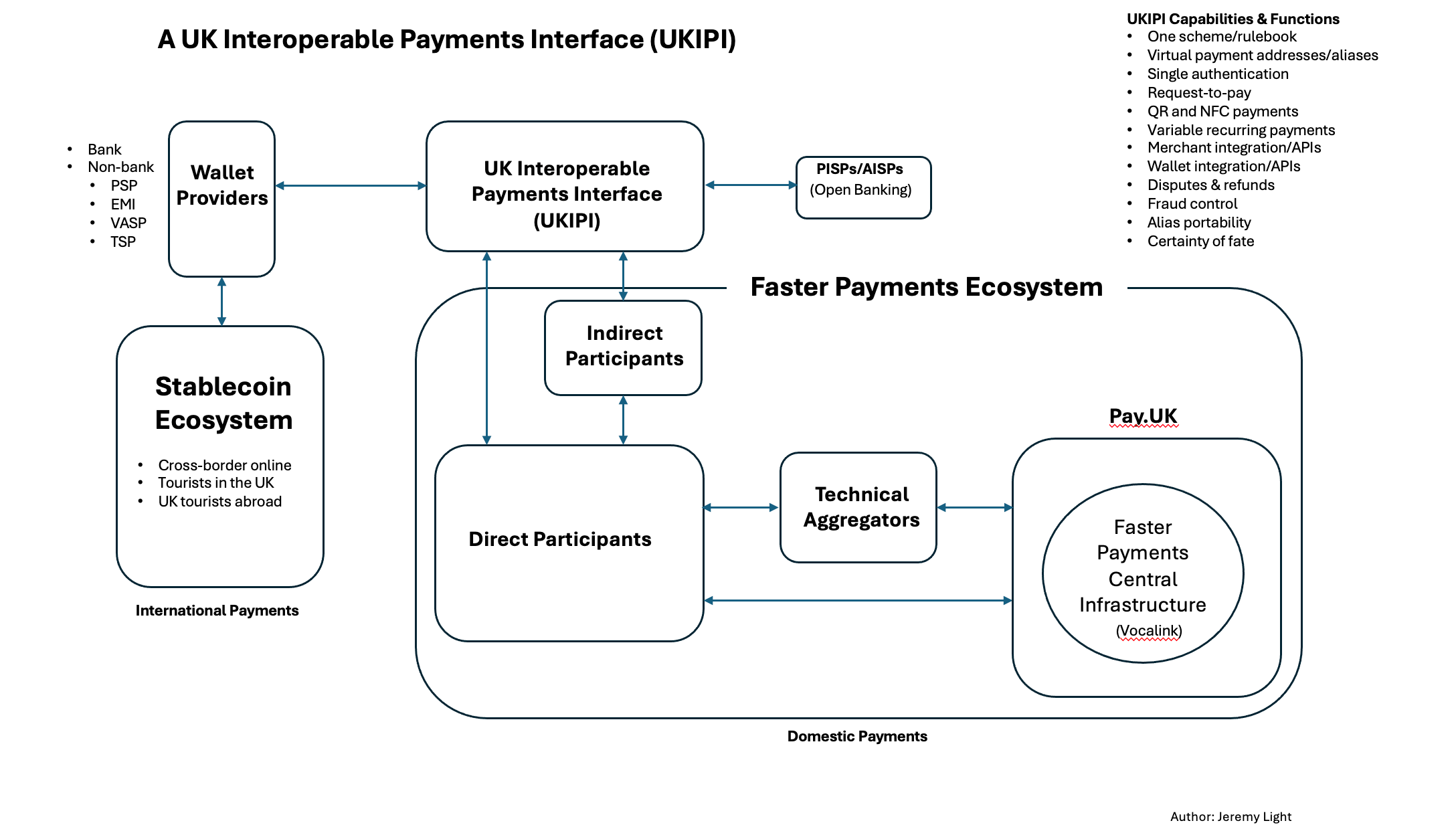

As I have hinted in the previous section, the biggest innovation FPS could enable is an overlay service similar to UPI in India. Figure 3 outlines how this might look, with a separate scheme and operation I have termed the “UK Interoperable Payments Interface (UKIPI)”, built for interoperability and inclusivity, to link into FPS, with open banking for domestic payments and with stablecoins for international payments.

Figure 3 – a UPI overlay for the UK?

Such an overlay service would open up UK payments to all players big and small, new and established, competing on a level playing field to provide wallet services, including real-time payments domestically and internationally. A core component would be a database of virtual addresses that allows any certified application or wallet with standard authentication to initiate and route payments from any bank or wallet to any other bank or wallet, enabling competition on wallet services and user experience.

If a service like UKIPI was implemented, it would generate 12bn transactions a year, double FPS current volume, if it were to match UPI on a per capita basis.

Overlay services are highlighted in the National Payments Infrastructure Strategy7, so expect to see more on them as the delivery of the National Payments Vision takes shape. Whatever form they take, user-centric overlay services are likely to be a key feature in the future of FPS.

The overlay service in Figure 3 is just one possible form, a later article on overlays will explain it in more detail, for the UK and more generically.

Conclusion

In this article and the previous two, I have explained FPS’s progress and successes since launch 18 years ago – it is an impressive story.

I would hope that Pay.UK and Vocalink mark its 18th birthday in style on 27 May 26 and raise a glass or two to themselves and all those who have made FPS an enduring success.

To-date, FPS has processed around 38bn payments and is likely to process a similar volume over the next five years. How it will be taken forward in the Interbank Infrastructure Renewal programme is unclear but for certain, for many years to come, FPS will keep on running.

Jeremy Light

Huge thanks to Jeremy Light for allowing Payments:Unpacked to feature “Keep on Running” as a guest blog.

Be sure to subscribe to Jeremy’s excellent Agenda: Payments newsletter at:

1 Real-time payments per capita index 2024:

2 Using my estimates for 2025 and UK Finance data for 2016.

3 Atomisation of payments:

4 Mozambique instant payments https://aimnews.org/2026/03/03/bank-of-mozambique-launches-instant-payment-system/

5 FPS certainty of fate rule clarification: https://www.wearepay.uk/wp-content/uploads/2026/01/Pay.UK-CoF-Proposed-Rule-Clarification-January-2026.pdf

6 Bank of England RTGS early morning extension: https://www.bankofengland.co.uk/paper/2026/ps/extending-rtgs-and-chaps-settlement-hours-early-morning-extension

7 National Payments Infrastructure Strategy: https://assets.publishing.service.gov.uk/media/690de7a247ad122f854627bf/PVDC_Strategy.pdf

Payments:Unpacked | On A (Slight) Tangent - Unscripted and unedited