How do you measure up?

The Future of Competitive Advantage in Banking and Payments Global Report

This week’s Payments:Unpacked is supported by Bottomline.

The Future of Competitive Advantage in Banking and Payments Global Report

Now in its fifth year, this report is built on a peer-based, real-time comparison benchmarking survey to see how executives and their companies are meeting customer expectations and progressing towards achieving their digital payments transformation strategy.

Topics covered include real-time/instant payments, cross-border payments, ISO 20022 messaging, transitioning from on-premises to SaaS, compliance and regulation, cash positioning and fraud monitoring, and payments verification. Includes insights from Accenture, PwC, Zanders, Payments Association, BNY, EBA Clearing, Open Banking Expo and Payments Unpacked.

Start Your Live 2026 Comparison Now!

Analysing these survey responses together makes it clear that banks are increasingly aligning their strategies with corporate needs. From fraud prevention and real-time payments to AI-driven solutions, there’s a visible shift from transactional operations to customer-centric, strategic partnerships.

What stands out is the focus on cash flow visibility, technology integration, and proactive innovation—demonstrating that institutions are not just responding to change, but shaping services that genuinely support corporate growth.

Mike Chambers, Payments:Unpacked

Dining out on acronyms… but what nearly was?

From Bacs to CHAPS, the UK payments industry has always had a talent for turning mouthfuls into memorable acronyms. But when a brand-new near real-time system was gearing up for launch in 2008, the naming stakes were higher than ever.

“Instant” didn’t quite fit. “Immediate” didn’t stick. And for a moment, the UK almost adopted a Scandinavian-inspired model that would have delivered little more than a “same day Bacs.”

So how did we end up with Faster Payments — and why was “S” left so conveniently flexible?

Click the link to discover the naming debate, the near-miss with ELLE, and the pivotal decisions that shaped the UK’s payments landscape.

Name and Shame: PSR Slaps £3.7m Fine on Bank of Ireland UK for Missing the CoP Memo

The UK’s Payment Systems Regulator has fined Bank of Ireland UK £3.7 million for missing the legal deadline to roll out Confirmation of Payee — a key anti-fraud control.

More than 1.14 million payments, worth roughly £6.9 billion, were processed without the safeguard in place after the 31 October 2023 deadline passed. The bank was the last major provider to comply, and while an early settlement reduced the penalty from £5.4 million, the regulator was clear: customers were left exposed to avoidable risk.

What went wrong, and what does this mean for firms under increasing regulatory pressure to tighten fraud controls?

Click through for the full story.

Payments Forward Plan

The Payments Vision Delivery Committee - comprising HM Treasury, the Bank of England, the Financial Conduct Authority and the Payment Systems Regulator - has published the Payments Forward Plan, setting out a coordinated roadmap of upcoming initiatives across retail and wholesale payments, including digital assets.

The Payments Forward Plan seeks to bring greater clarity on timing and priorities, supporting firms to plan investment and innovation while advancing the Government’s National Payments Vision for a trusted, technology-enabled and globally competitive payments ecosystem.

It highlights the breadth of ongoing activity, from open banking developments to stablecoins and contactless policy, and confirms that payments will receive enhanced focus in the 2027 Regulatory Initiatives Grid.

We’ll be publishing a more detailed analysis of the Payments Forward Plan and its implications for the sector shortly.

Bank of England to Launch 1:30am Start for CHAPS

The Bank of England has announced that it will lengthen operating hours for the UK’s high-value payment system, CHAPS, introducing a new early-morning settlement window beginning in September 2027.

Following industry consultation, the central bank confirmed that the CHAPS settlement day will commence at 01:30, replacing the current 06:00 start time.

Participation in the additional window will be voluntary, allowing direct CHAPS members to submit payments during the newly created early-morning period.

According to the Bank, the extension is intended to:

Enable earlier Sterling settlement

Enhance liquidity management

Improve operational resilience

Better synchronise UK settlement cycles with global financial markets

There are no immediate plans to lengthen the evening contingency window. However, the Bank confirmed that work continues on proposals covering bank holiday settlement and the broader transition toward near-24/7 settlement capability.

A further consultation paper outlining the next phase of reforms is expected in Spring 2026.

UK Payments Initiative Confirms Initial Pricing Framework for Commercial cVRP Scheme

UK Payments Initiative (UKPI) has confirmed its initial pricing framework for participation in the commercial Variable Recurring Payments (cVRP) scheme, marking a significant step in the development of a sustainable account-to-account payments model aligned with the UK’s National Payments Vision.

As an industry-led body established to create a commercially viable alternative to cards, UKPI is focused on enabling new payment journeys, fostering innovation and building a trusted ecosystem for participants, retailers and consumers. For

Wave 1 of cVRP transactions, the framework sets a 2.5p scheme transaction fee payable to UKPI and shared equally between ASPSPs and PISPs (1.25p each), alongside a 5.5p access fee payable by the PISP to the ASPSP for each successful payment.

The pricing structure, informed by detailed economic analysis, is intended to encourage early adoption while supporting a scalable and sustainable long-term model. An annual membership fee of £5,000 will apply in the first year of participation.

In line with the government’s Forward Payments Plan, also published today, this represents the first phase in delivering secure and streamlined payment options across the ecosystem, spanning future use cases from flexible bill payments and peer-to-peer transfers to point-of-sale and ecommerce transactions.

When a Banking Hub comes to town

Understanding Certainty of Fate in Faster Payments

Insights from Pay.UK and Open Banking Limited

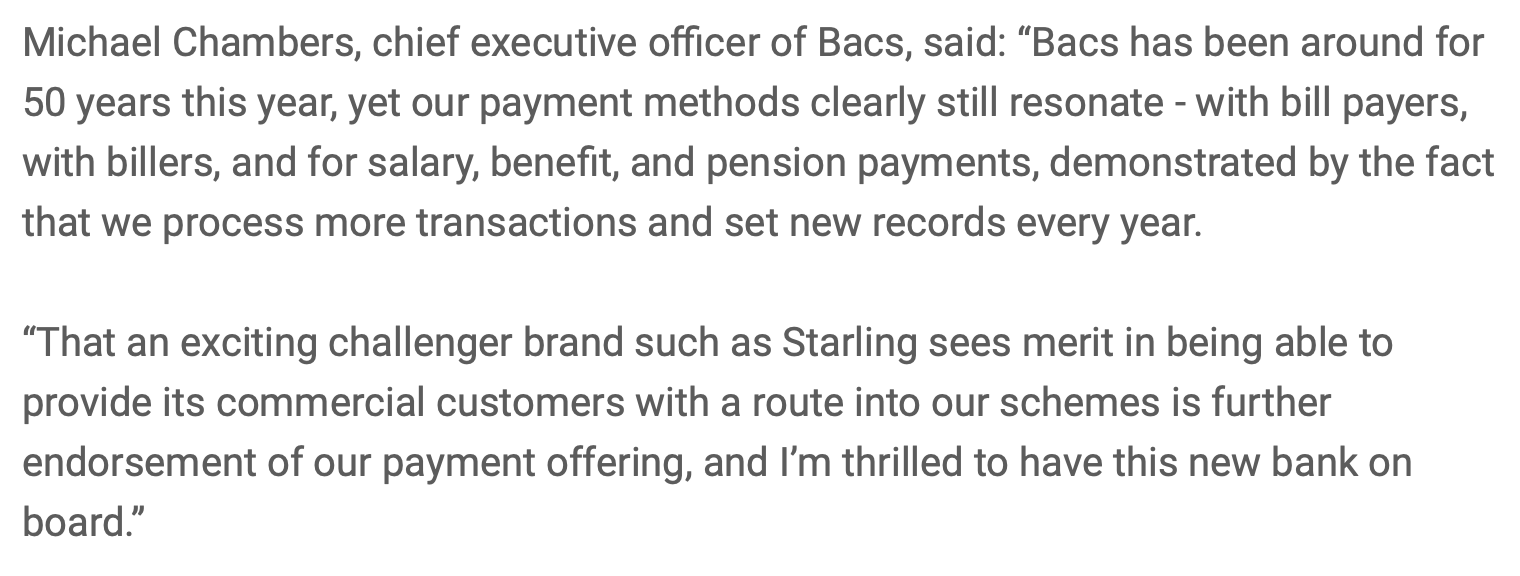

On this day: 27 February 2018

OTD in 2018 I announced that Starling Bank had become a direct participant in the Bacs schemes:

Subscribe