Five things you need to know about acquiring cash

Issue 659: 22 October 2024

Source: LINK

Cash access for all

The LINK scheme processes an average of 4 million cash withdrawals and balance enquiries every day and ATMs account for around 90% of cash acquisition in the UK.

Here’s five things you ought to know about LINK from their just published annual report. You can download LINK’s 2024 Annual Report here.

1: Universal access to cash in a safe, convenient and rapid manner

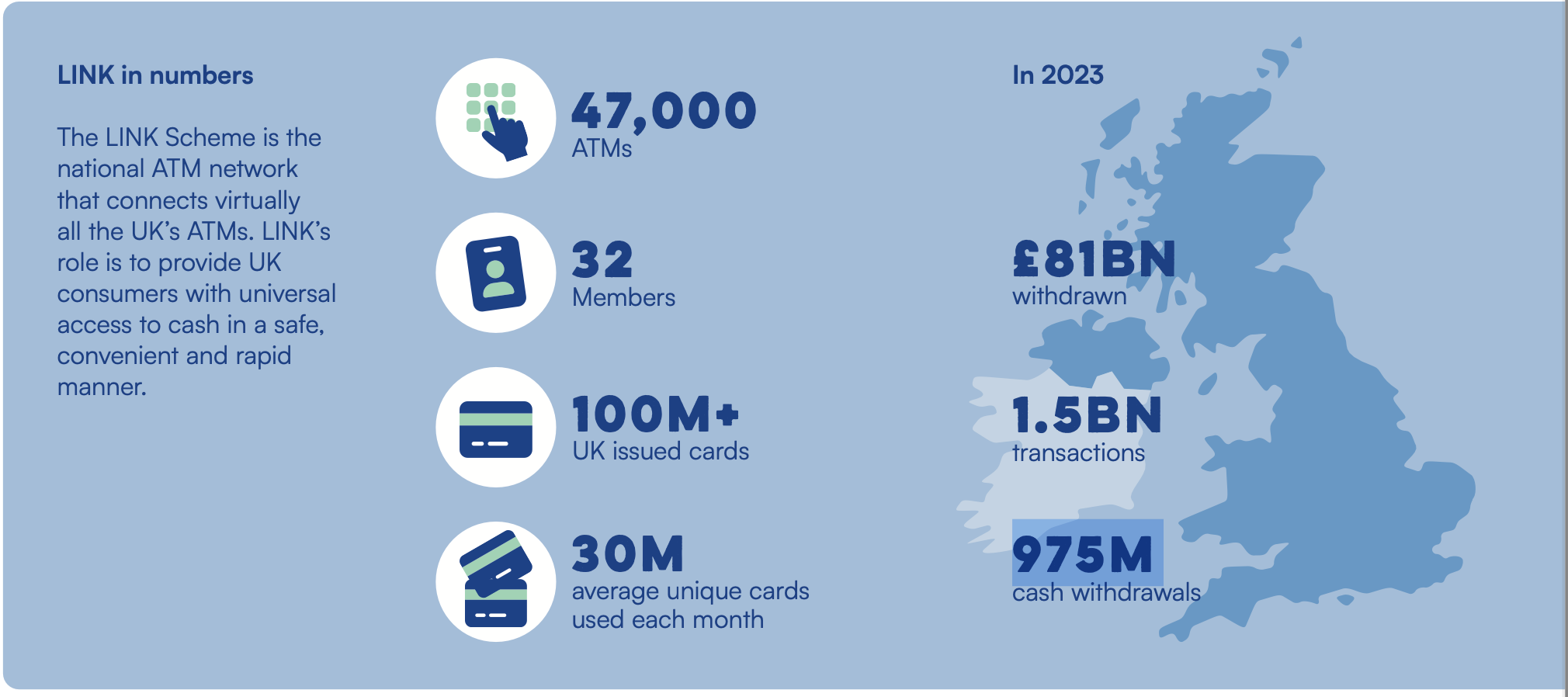

Source: LINK

The LINK Scheme is the national ATM network that connects virtually all the UK’s ATMs. LINK’s role is to provide UK consumers with universal access to cash in a safe, convenient and rapid manner.

LINK’s research shows that, while most consumers are increasingly happy to use cards or phones for their day-to-day payments, they also want cash to continue as an option for payments.

Sir Mark Boleat, Chair, LINK

2: Link has four key objectives

Source: LINK

The LINK Strategic Plan, updated in early 2023 to cover the period until end-2024, is built around objectives that address the challenges that LINK faces. Delivering access to cash for UK consumers for as long as they need it is the focus of the access to cash objective. Maintaining confidence in the LINK Payment System is the focus of the operational resilience and risk management objectives. Retaining the support of LINK’s Members, without which LINK cannot exist, is the focus of the membership objective.

Ensuring consumers can continue to access their cash, in the face of an overall decline in cash use and increasing commercial pressures on the industry, is LINK’s key objective.

John Howells, CEO, LINK

3: ATM Use

Source: LINK

ATMs continue to dominate consumers’ cash acquisition, accounting for 91% by volume and 89% by value of all cash acquisition in 2023. This means that in the absence of any new technical innovation such as a new widely accepted person-to-person payment app, or some other transformational event, ATM transactions in 2033 will be 45% down on 2023’s and 75% down on what they were a decade ago. However, this also means there will still be significant demand for cash and over 800m ATM transactions a year.

There are some variable factors at play when forecasting total ATM transactions which should not be forgotten, especially over a 10-year time horizon. Firstly, around 30% of total transactions are still balance enquires, which is not insignificant. While this ratio has remained broadly the same for many years, a collapse in balance enquiries, for example if consumers moved wholesale to some other channel, would have a significant effect on total ATM transactions.

Another potential variable is the average value of each cash withdrawal. Since the pandemic, the average withdrawal value has increased from £67 to £84 today. If this trend continues, then it is possible at least some consumers will be visiting ATMs less but still satisfying the forecast demand for cash payments that LINK is using as a guide. This could reduce the number of transactions further, even if the actual value of cash being dispensed and used by consumers remained as forecast.

Therefore, consumers using less cash, visiting ATMs less often, but taking out more cash when they do is the post- pandemic pattern.

Graham Mott, Director of Strategy, LINK

4: ATM Numbers

Source: LINK

There are currently around 36,500 free-to-use ATMs in the UK, of which 10,500 are in branches and 26,000 are remote. The total number of free machines has fallen by around 6% in the past year and by 19% since January 2020. LINK is currently forecasting there to be around 20,000 free-to-use ATMs in 2032.

Excepting a blip in 2019, the number of charging, pay- to-use ATMs has been in steady decline for many years and LINK expects this trend to continue. Consumers’ free access to cash remains, and will remain, good. While there may be occasions where people want to pay for cash for convenience or to spend locally (for example an ATM in a pub), the number of locations which don’t accept card payments is getting smaller all the time and therefore the number of occasions when consumers need cash and there isn’t a free ATM available will be getting less and less.

LINK will ensure that these ATMs are in the right locations, if necessary by subsidising some machines and even directly managing other ATMs’ installation and ongoing management.

Graham Mott, Director of Strategy, LINK

5: Financial Inclusion

Source: LINK

In a world that is becoming dominated by digital payments, LINK’s Financial Inclusion Programme ensures that consumers can continue to access cash for as long as they need it.

There is a huge crossover between people who are digitally excluded and people who still rely on cash.

LINK

LINK Annual Report 2024

Download LINK’s 2024 Annual Report and dig deeper than these five key facts.

Keep reading with a 7-day free trial

Subscribe to Payments:Unpacked to keep reading this post and get 7 days of free access to the full post archives.