Developments at Pay.UK, PSR, BoE, HMT and Open Banking

Developments at Pay.UK, PSR, BoE, HMT and Open Banking

Issue 88 | 15 January 2021

Welcome to issue 88 of Payments:Unpacked, this premium subscriber edition provides a fortnightly round-up of developments at Pay.UK, the Payment Systems Regulator, the Bank of England, HM Treasury and the Open Banking Implementation Entity.

Period covered: 1 January to 15 January 2021.

Pay.UK

Fast forward to 2030: Retail payments in a future world

On the 26 January Pay.UK are holding a webinar titled “Fast forward to 2030: Retail payments in a future world.”

The webinar will consider long term strategic trends shaping the payments market out to 2030 based on Pay.UK’s research, the key drivers of immediate change, and what impact the Covid-19 pandemic has had.

Pay.UK understands that people and businesses everywhere want payment services that are safe and secure, easy to use, and flexible to meet the challenges of a changing world. We’re inviting you to join us in considering the opportunities and drivers that will shape the consumer payment behaviours of the future.

Pay.UK say that the discussion will include:

The nine payment trends identified by Pay.UK that are set to shape the payments market of the future.

How Covid-19 will impact key drivers – atomisation, internalisation and virtualisation.

How you can join the conversation about the future of payments by participating in Pay.UK’s first industry challenge.

Kate Frankish, Director of Strategy and NPA Product Owner at Pay.UK, will lead the discussion and will be joined by panellists:

Eddie Keal – Also a PAC member as well as Banking & Financial Markets Industry Leader at IBM

Arunan Tharmarajah – Head of European Banking at Transferwise.

For more information and to register visit: Fast forward to 2030: Retail payments in a future world.

Financially vulnerable could miss best deals and require more support to switch bank accounts

Latest Pay.UK research indicates that financially vulnerable consumers would benefit from more targeted information and support to overcome negative associations with switching (Frontier Economics research commissioned by the Current Account Switch Service).

The long-term impact of the COVID-19 pandemic could potentially lead to sustained higher levels of financial vulnerability for some time. It is vital those who could benefit from switching have access to information that allows them to fully understand the process. That is why we are committed to continue to raise awareness among this group.

Our research partnership with Frontier Economics has generated a number of findings for the switching ecosystem to consider. It suggests that the whole current account ecosystem has a role to play in ensuring people can switch if they want to, when they want to. The Current Account Switch Service is committed to collaborate with current account providers and consumer representatives to facilitate the work needed to review and refresh the switching service.

Maha El Dimachki, Chief Payments Officer of Pay.UK, owner and operator of the Current Account Switch Service.

More (including the full report): CASS Research.

Reduce customer effort, drive loyalty and reduce customer churn with Request to Pay.

A perspective from James Stanley, Collections Campaign Strategy Manager, Anglian Water.

….what do we mean by customer effort and how can Request to Pay help with this challenge? In the Harvard Business Review article Stop Trying to Delight Your Customers, one of the critical findings was that delighting customers doesn’t build loyalty; reducing their effort—the work they must do to get their problem solved—does. In simple terms, organisations that make it easy for customers are more likely to retain that customer in the longer term. So how can Request to Pay help?

James Stanley, Collections Campaign Strategy Manager, Anglian Water

More: Request to Pay - a perspective from James Stanley.

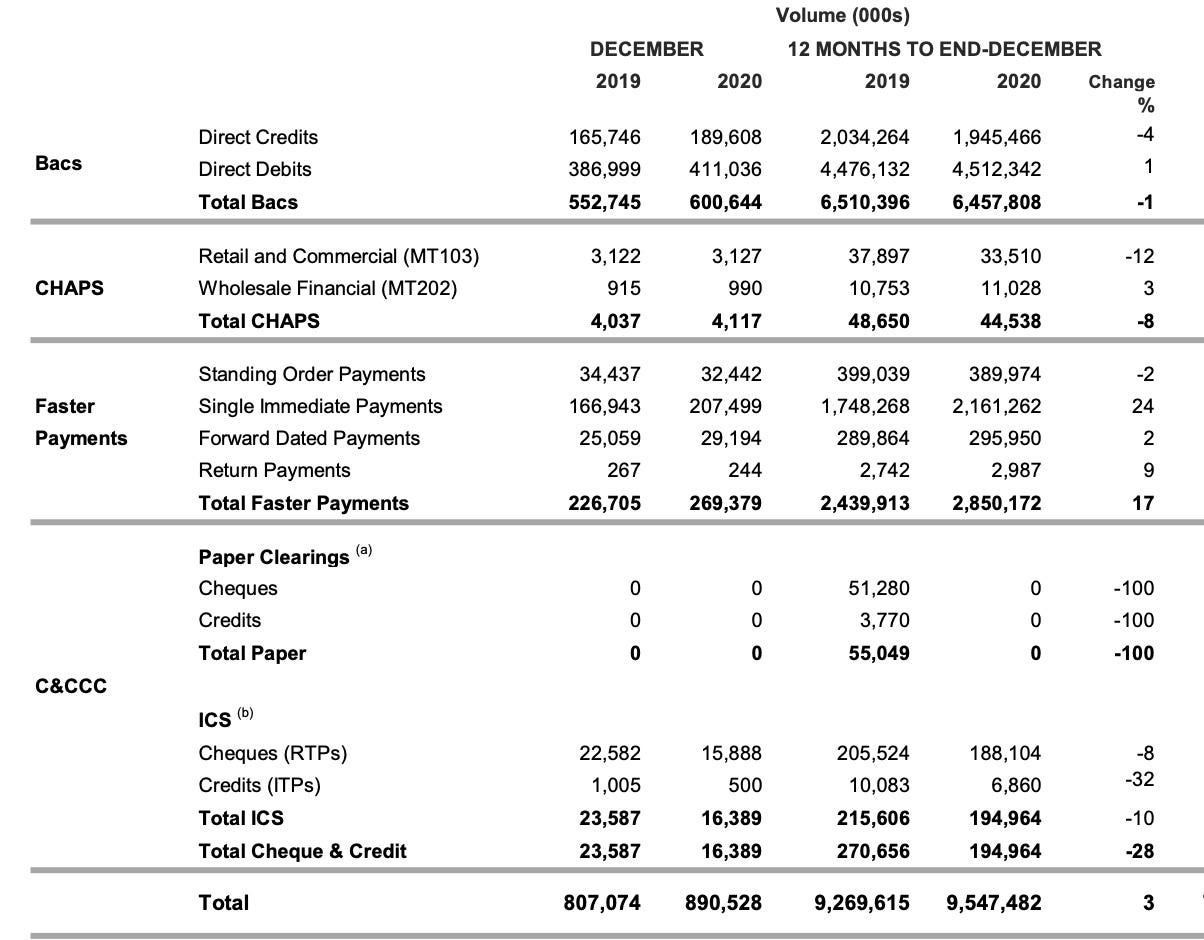

Retail payment statistics:

December’s retail payment statistics have just been published at: Retail payments December 2020.

You’ll find our analysis of this data at: Northey Point: Payments Tracker (Note: December’s analysis will be posted over the weekend) - but here is a snap shot of the UK’s retail payments landscape by numbers at the end of 2020:

Source: Pay.UK

Payment Systems Regulator (PSR)

Specific Direction 8 (SD8): LINK

On the 14 January the PSR announced that they were opening their second review of Specific Direction 8 (SD8), which they gave to LINK in October 2018, to ensure it fulfilled its public commitment to maintain the broad geographic spread of free-to-use ATMs and stated that they would like to hear views on how well SD8 is working in practice.

However today (15 January), the PSR have advised that there are some things that they would like to double check before they seek input and the web-page has been temporarily “unpublished”.

Bank of England (BoE)

Nothing to report.

HM Treasury (HMT)

Nothing to report.

Open Banking Implementation Entity (OBIE)

A remarkable achievement and still only the beginning

It has been three years since PSD2 marked the start of Open Banking, the UK has built a world-leading ecosystem.

The OBIE report that over the last three years:

300 fintechs and innovative providers have joined the ecosystem

More than 2.5 million UK consumers and businesses now use open banking-enabled products to manage their finances, access credit and make payments.

Every month, hundreds of thousands of UK consumers and businesses become new active open banking users

API call volume has increased from 66.8 million in 2018 to nearly 6 billion in 2020.

Open banking used to be the best kept secret in financial services. We have worked hard to develop the open banking infrastructure and functionality over the past three years and our significant progress is reflected, not only in the millions of active users of open banking technology each month, but in the sustained momentum of growth we are seeing. We have developed a world-leading, thriving ecosystem of nearly 300 regulated providers, who collectively are bringing innovative new products and services to market.

Imran Gulamhuseinwala OBE, Implementation Trustee, The Open Banking Implementation Entity

Three years ago, we ordered banks to give people control of their own data to help transform the industry, driving innovation and stimulating rivalry. Today, more than two and a half million people are using open banking, with new customers coming on board every day. This is a remarkable achievement and still only the beginning for how far we can take this technology.

CMA spokesperson

More:

Three years since PSD2 marked the start of Open Banking, the UK has built a world-leading ecosystem.

The third anniversary of Open Banking in the UK: A cause for celebration?

And finally:

"Why we need to stop the Klarnage" - UK Government votes down bill to regulate BNPL firms (Source: Finextra).

The UK Government has voted down a bill supported by 70 MPs to regulate buy now, pay later firms like Klarna, Laybuy and Clearpay.

The amendment to the financial services bill was sponsored by Labour MP Stella Creasy, who referred to the entry of a host of BNPL firms as the "next Wonga waiting to happen".

The BNPL industry has seen huge growth in recent years, with the likes of Klarna and Affirm becoming multi-billion dollar giants.

According to research by Credit Karma, a quarter of Brits used buy now, pay later services to fund Christmas shopping, setting up a £2.3 billion bill.

A recent study by Capco reveals that more than half of 18-34 year olds using it have missed a payment and nearly two thirds say it is making them spend more, potentially increasing their chances of getting into debt.

The Financial Conduct Authority is conducting a review into buy now, pay later firms, but some MPs worry that the lengthy process could push regulation out by another 18 months, leaving consumers drowning in debt during an economic downturn.

Creasy express disappointment in the Commons vote in a video posted on twitter headlined "Why we need to stop the Klarnage".

Read, subscribe and share

This Payments:Unpacked ‘regulatory’ round-up is issued fortnightly to Premium newsletter subscribers - next round-up due: 31 January 2021.

Why not share this round-up with your colleagues:

If you work for an organisation that is a client of Northey Point then select the ‘free’ subscription membership option and your subscription will be upgraded.

Mike