ScamClassifier

Today’s Payments:Unpacked is brought to you by Wavestone - the largest independent consulting firm in Europe.

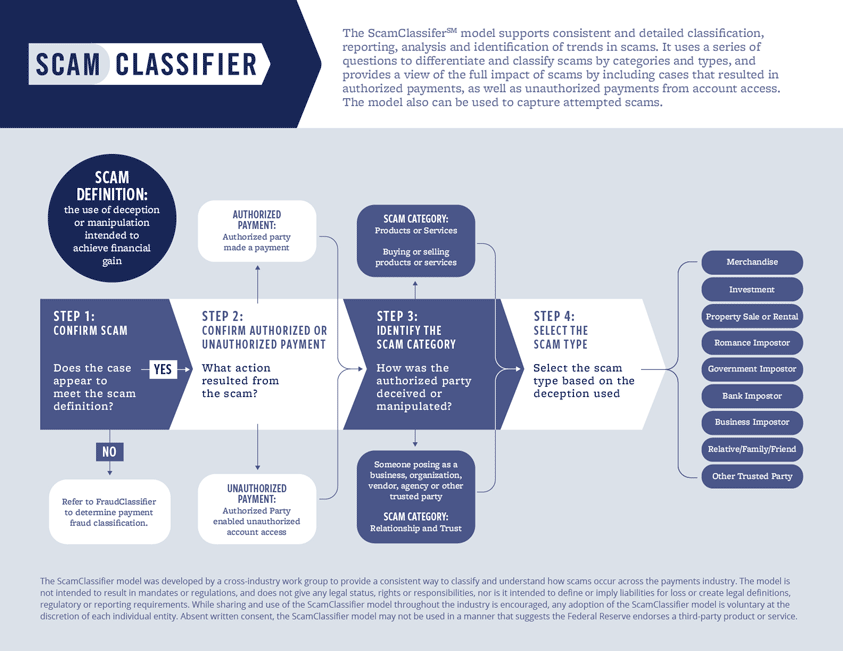

Fed launches ScamClassifier model

The Federal Reserve has developed a tool, called the ScamClassifier model, to help the payments industry improve scam reporting, detection and mitigation.

Last year, more than $10 billion in consumer fraud losses were reported to the Federal Trade Commission, up 14% on 2022.

The ScamClassifier model uses a series of questions to differentiate and classify scams by category and type.

The Fed says that by using the model, the industry can improve the focus for detection, investigation and mitigation; expediate scam claims intake; and improve reporting.

We are seeing a groundswell of support for fighting this type of fraud - and the ScamClassifier model can help us do so through better classification and reporting. Mike Timoney, VP, payments improvement, Federal Reserve Financial Services.

Meet Elle - the alternative Faster Payment

Did you know that the UK nearly ended up with an alternative to Faster Payments?

Let me introduce you to Elle.

You'll see that the UK would have been much poorer with Elle.

Before 2008 payments were a real pain - this all changed when Faster Payments entered our lives.

Faster Payments has transformed who we pay, how we pay and when we pay - socks, last nights pizza and household appliances can now be bought within seconds via a smartphone.

Remembering a time when payments could take days is like trying to recall what it was like to travel via a house and carriage.

Find out how we avoided the distraction of Elle and found a new way to pay:

Digital euro would maintain freedom to choose how Europeans pay

With Europe inching towards the issuance of a digital euro, the ECB has embarked on a charm offensive to reassure citizens that the new payments option will compliment, not replace, cash and provide them with greater freedom of choice.

While a final decision on issuing a digital euro has yet to be made, the ECB last year moved onto a two year preparation phase ahead of any launch, which would come in 2026 at the earliest.

Making the case for a digital currency here’s four quote from ECB executive board member Piero Cipollone:

“We do not yet have a cash equivalent for making digital payments, which limits our freedom in an increasingly digital age.”

“A digital euro would combine the convenience of digital payments with cash-like features" - adding that it could be used in shops, for e-commerce, P2P payments and offline.

"The digital euro would make it easier for euro area firms to offer pan-European digital payment solutions. This would strengthen competition in a market currently dominated by a few non-European players, thereby lowering costs for merchants and consumers."

"More than just a payment option, a digital euro would bring Europeans closer in an increasingly digital and unstable world. It would make our lives easier, while preserving our freedom of choice,"

Going ISO 20022 Native

Insurance coverage against APP fraud

Elmore Insurance Brokers and RegTech Green Swan Compliance have teamed up on the development of an Authorised Push Payment (APP) Fraud Reimbursement Insurance product for qualifying UK banks, Payment Service Providers, E-Money Institutions, and Authorised Payments Institutions.

The UK's Payment Systems Regulator is pushing plans to improve protections for victims of APP fraud that will see the vast majority of money - up to £415,000 - lost to APP frauds reimbursed to victims. Despite industry pushback, the new rules are set to come into force in October 2024.

To help firms mitigate risk and protect balance sheets from any adverse effects from the new regulations, Lloyds broker Elmore and Green Swan have collaborated on the development of a new APP insurance product to protect UK financial institutions processing Faster Payments.

2025 - 2030: Predictions for Real-Time Payments, ISO20022 and APIs

At EBAday 2024, Akshat Saharia, Head of European Financial Institutions Product and Propositions, Global Payments Solutions, HSBC discusses the biggest changes to occur across the cross-border payments landscape in the next five years.

While 90% of cross-border transactions complete in 30 mins, the other 10% can be delayed, resulting in frustration and a lack of transparency.

Robust change will be seen with real-time payment schemes opening up for cross-border payments. In turn, with ISO20022 being mandated from November 2025, banks in the world will be operating with enhanced data, standardised information and LEIs which will significantly enhance STP and reduce costs.

Digital transformation through the use of APIs will also bolster end-to-end connectivity, paving the way for value-added services offering increased transparency and verification with Confirmation of Payee.

In brief

Barclays, HSBC and Nationwide customers hit by payment delays.

Visa launches digital card replacement service for travellers

Wearable paytech provider MuchBetter has launched a contactless payments ring in Italy that is free - as long as users load it with €100 through the associated app.

The Swiss National Bank is to expand its wholesale central bank digital currency pilot, Helvetia, for a further two years after promising results in early trials.

Vipps MobilePay launches P2P payments between Denmark, Norway and Finland.

The difference between Direct Debit vs Recurring Card Payments by Movimo.

Today’s Payments:Unpacked is brought to you by Wavestone

Wavestone is the largest independent consulting firm in Europe which deploys highly experienced consultants to work with its clients to deliver lasting change on their most complex transformation issues.

Enhance your payments knowledge