Outpacing the fraudsters

Outpacing the fraudsters

Issue 628: 3 July 2024

Today’s Payments:Unpacked is brought to you by Bottomline - 13 quick questions to get instant visibility on how your strategy and pain-points compare with your peers in banking and payments.

A trio of new fraud controls from Monzo

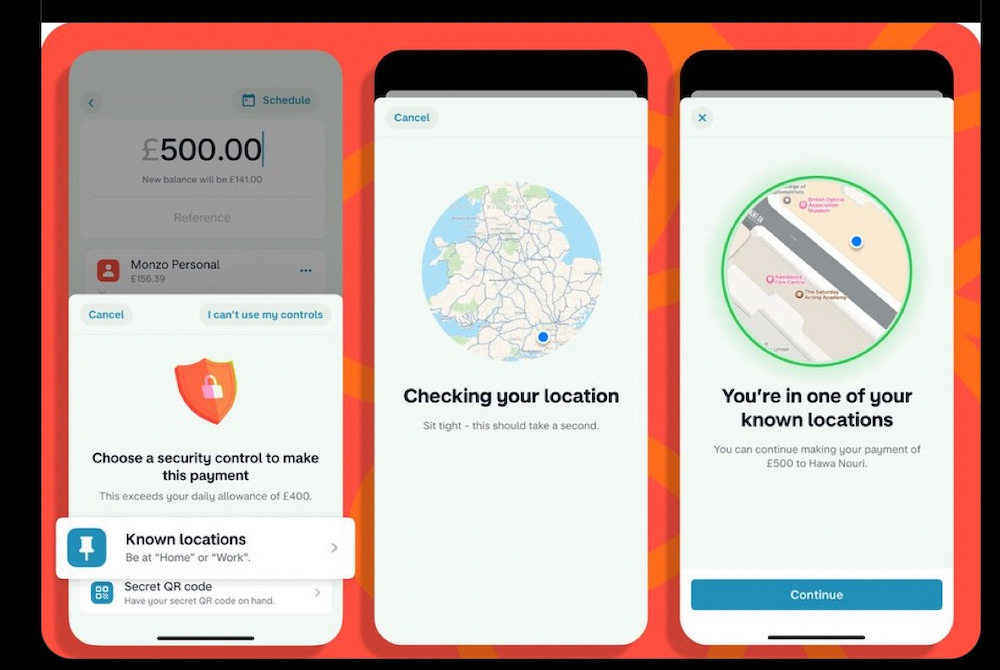

Monzo has introduced a trio of security controls to help customers reduce the prospect of fraudulent payments out of their accounts from phone theft, shoulder surfing or impersonation scams.

The controls, which are called Known Locations, Trusted Contacts and Secret QR codes, are opt-in for customers and will be rolled out over the coming weeks. Customers need to have at least two of these controls set up and can choose the limits at which each control is activated when making bank transfers or instant access savings withdrawals from pots.

For Known Locations, customers choose places like home or work that they need to be in when making bank transfers or savings withdrawals over their chosen limit. If they are outside of their chosen known location, the transfer will not complete.

Customers can also invite a trusted friend or family member who uses Monzo to help check whether a transaction over their chosen limit looks safe or is suspicious before they make the transfer or savings withdrawal.

Secret QR codes can be stored on a different device and must be used in parallel with the user's phone to approve a payment or savings withdrawal over their chosen limit.

As fraudsters become more and more sophisticated we’re continuing to invest to outpace their tactics and keep our customers’ money safe. Whether it’s choosing your safety radius with Known Locations or having a trusted contact sense-check your payments before you make them, these features offer customers peace of mind and force a much-needed moment of pause in a high-stakes situation.

Priyesh Patel, senior staff engineer at Monzo

National Payments Vision

In 2023 His Majesty's Treasury (HMT) commissioned a review to consider how payments are expected to be made in the future, and to offer recommendations on the next steps to successfully deliver world-leading retail payments.

Authored by Joe Garner, former CEO of Nationwide Building Society, the ‘Future of Payments Review’ was published in November 2023 as part of the Autumn Statement.

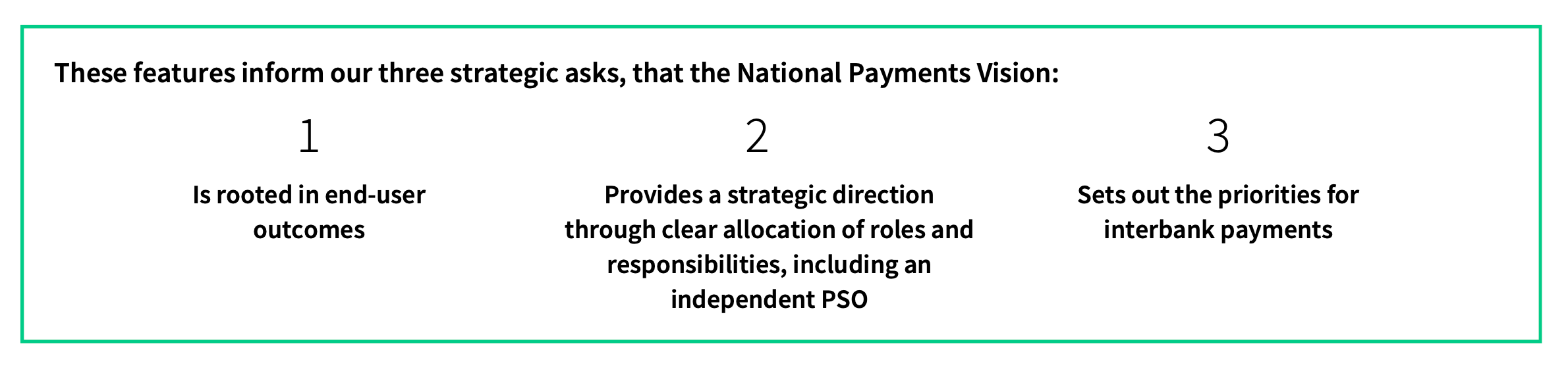

Picking up on the review’s primary recommendation forward – that the Government should develop a National Payments Vision and Strategy outlining its ambition and the shared outcomes it wants to achieve - Pay.UK have published a viewpoint on how this vision can create the conditions for UK interbank payments to thrive.

Pay.UK’s research has identified that there are four essential features of a successful payments eco system:

Source: Pay.UK

From these four essential features of a successful payments eco system Pay.UK have identified three strategic asks of the National Payments Vision:

Source: Pay.UK

Read Pay.UK’s viewpoint: Pay.UK’s view on the National Payments Vision.

Competitive advantage in banking and payments

How do you measure up in meeting customer expectations and in your digital payments transformation strategy?

Answer 13 quick questions to get instant visibility on how your strategy and pain-points compare with your peers in banking and payments.

Additionally, receive a personalized infographic and report summarizing the results ensuring you are one of the first to access the final report in October 2024.

Thought-provoking questions, and I appreciated seeing the total results by question and how my opinion compared to the rest of the respondents.

Olimpia Modorcea, Euronet Worldwide

Why is the survey worth taking?

The simple answer: Competition.

It is vital for banks and FIs to take advantage of the opportunity to compare their strategic priorities, product roadmaps, and plans for future innovation with their peers. In the process, they could discover the technology trends the industry is prioritizing and ensure they are aligned.

This global report from Bottomline is now in its fourth year and in 2023 they received results from almost nine hundred banks and FI players across Treasury, Fraud, Operations, Product, and C-Level in 34 countries globally, and are on track to double this in 2024.

The question is can you afford not to take the survey?

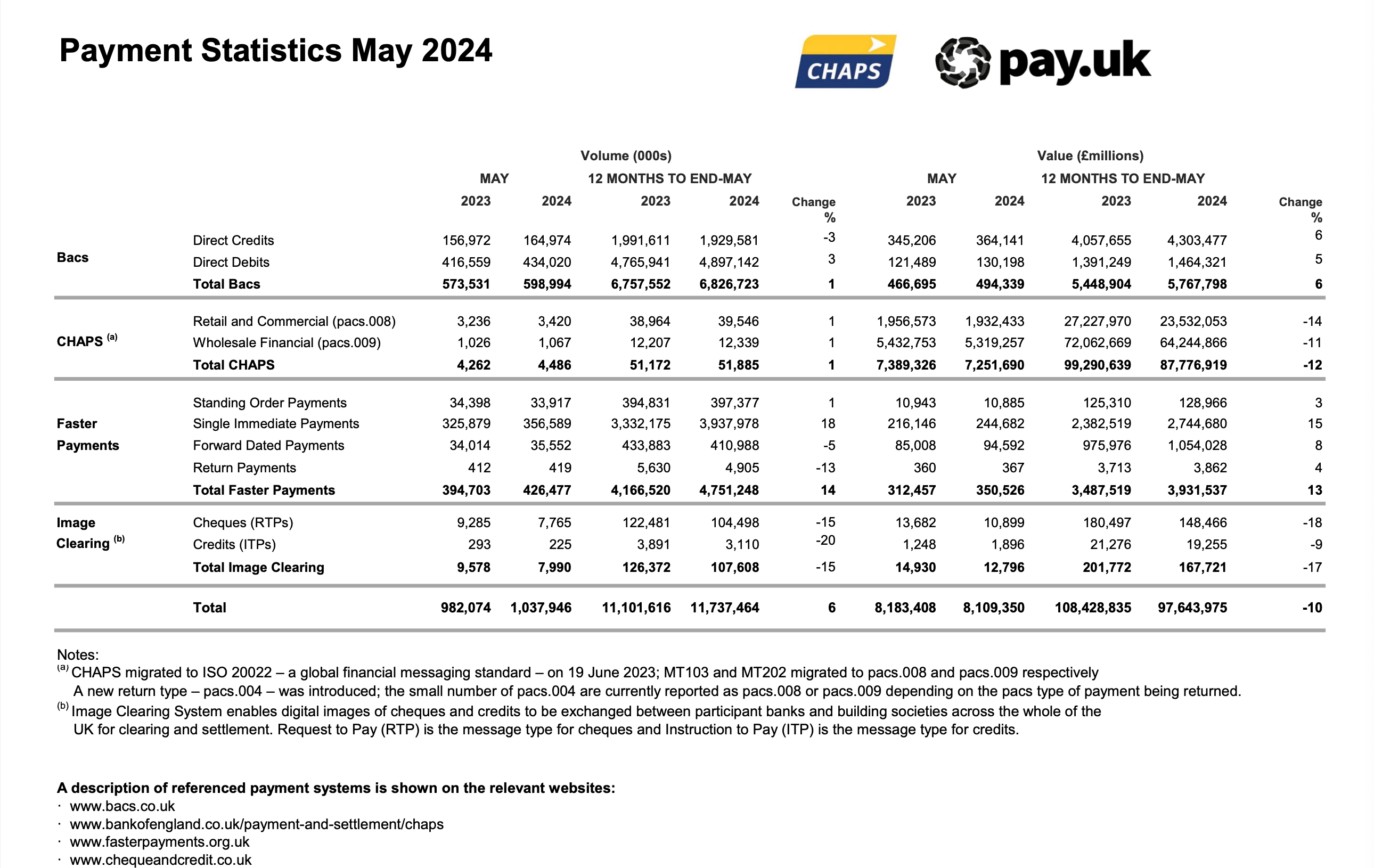

Statistics: UK’s retail payment rails

Five key facts for the 12 months ending May 2024:

14% growth in Faster Payments.

15% decline in cheque clearing.

4.9 billion Direct Debits were processed (+3%).

6% net growth in total volumes processed (11.7 billion transactions).

10% decrease in value of transactions processed.

EPI launches wero wallet in Germany

The European Payments Initiative (EPI) has launched its mobile-first wallet and instant account-to-account payments system in Germany, with other counties set to follow in the coming months.

German Sparkassen and Volksbanken, Raiffeisenbanken customers can now make instant money transfers from account to account between individuals, via their banking app. Deutsche Bank will launch wero later this year, starting with Postbank.

The wallet will be available in Belgium by the end of July for KBC customers before arriving in France this Autumn and coming to all EPI bank members within the next six months.

EPI is a Europe-wide bank-backed venture that was initially set up to build a rival to Mastercard and Visa on the continent, offering a card for consumers and merchants, a digital wallet and P2P payments.

Initially backed by 31 major Eurozone banks, the project was forced to reassess when half its members - including Germany's Commerzbank and DZ Bank - left in 2022.

Since then, EPI has acquired Dutch payment scheme iDeal and Luxembourg's Payconiq as the foundation for the wero wallet, beginning with P2P payments.

Next year, wero will get the ability to pay any small professional from the wallet, and also pay merchants online and upon invoices via QR code. This includes the ability for consumers to manage recurring payments for subscriptions or installments, but also to pay in merchant apps at point of sale without going through the cashier.

European Instant Payments Regulation: Are Banks Ready?

At EBAday 2024, Kjeld Herreman, Head of Strategy Advisory, RedCompass Labs, discussed the fast approaching deadlines and how financial institutions can be best prepared for the SEPA instant payments regulation.

The conversation explores how the deadlines are short, with just nine months to ensure banks are receiving instant payments and 18 months to send instant payments.

Further, ensuring Verification of Payee operates across all channels is a colossal task and with banks no longer able to charge for instant payments, the industry can expect hundreds or even thousands of friction-free transactions per second, but a lot of work needs to be completed before that point can be reached.

In brief

China’s bank branches, ATMs dwindle amid e-payments and cashless shift.

Five Asian markets to link domestic instant payment schemes.

Today’s Payments:Unpacked is brought to you by Bottomline

With the ISO 20022 Co-existence period underway since March 2023, extending until November 2025, and 19% of global cross-border payments traffic on Swift already utilising ISO 20022 as of December 2023, the momentum towards this universal messaging standard is palpable.

Now is the time to talk to Bottomline.

Enhance your payments knowledge