Open Banking's next step: Variable Recurring Payments

Open Banking's next step: Variable Recurring Payments

Issue 620: 6 June 2024

Today’s Payments:Unpacked is brought to you by Card Industry Professionals | UK Card Payment Solutions. Over the coming weeks you’ll find some extra Payments:Unpacked material on YouTube - subscribe today so you don’t miss out.

Open Banking’s next step: Variable Recurring Payments

Finextra have just published an excerpt from the Future of Digital Banking in Europe 2024 report focussing on why variable recurring payments might be the next step in growing European open banking.

VRP builds on open banking technology, they are open banking’s next step. VRP act similarly to direct debits, transferring money from one account to another at regular intervals under specific mandates set by the payer. However, unlike direct debits, they settle in real time, account details do not need to be shared, and are customisable.

There are two main types of VRP, sweeping and commercial. Sweeping VRP is currently available in the UK and are not yet available in Europe.

Finextra not the that the UK is leading the way in this area, with the Competition and Markets Authority (CMA) already mandating the CMA9 (Lloyds, Barclays, Nationwide, RBS, Santander, Danske Bank, HSBC, Allied Irish Bank and Bank of Ireland), are to implement VRP. This means Europe could learn from the steps that the UK makes, allowing them to build on any of the successes, or failures, seen in sweeping VRP.

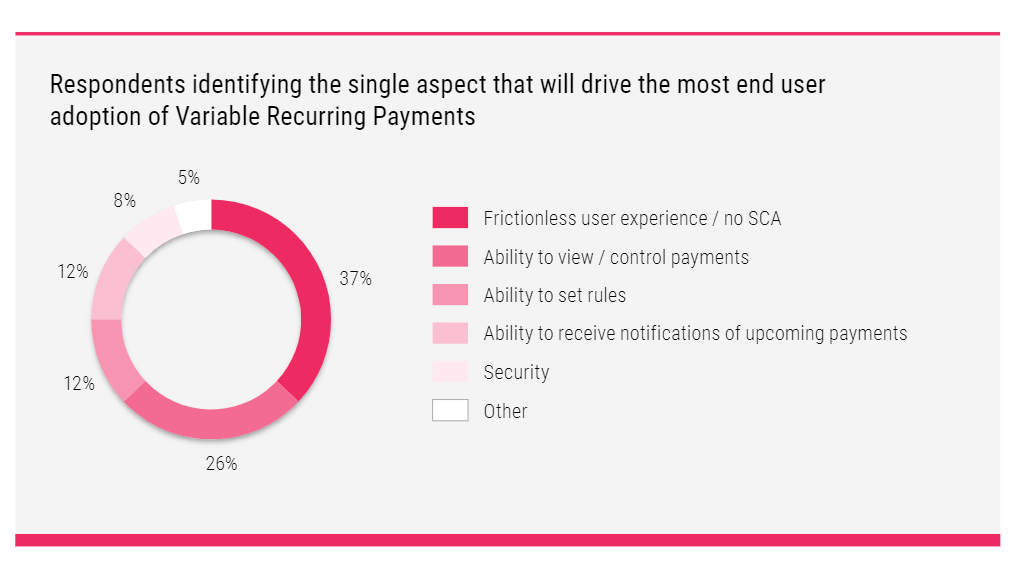

A survey by Token.io, in the diagram above, highlights the benefits of VRP which senior leaders from banks, merchants, payment providers and technology providers saw. However, for both Boyajin and Simoneschi, the real benefits of VRP are seen in the use cases created through commercial VRP.

More: Open Banking next step: Variable Recurring Payments.

Confirmation of Payee: Which model is best for you?

Rising to the fraud challenge

Open Banking Expo and Bottomline have published a new report, ‘Rising to the Fraud Challenge 2024’, which takes a deeper dive into the fraud landscape through key industry statistics and critical insights on fraud monitoring and prevention from Pay.UK, as well as senior executives at Bottomline.

Download your copy of the report to find out more and read fresh perspectives from key industry experts and Bottomline executives.

Also:

Enhancing fraud prevention strategies – the value of integrated solutions.

UK Finance: Next UK government should make Big Tech pay to fight scams.

Pay.UK hails fraud detection pilot results

UK trials 'super ATM' that will accept deposits for multiple banks

The UK's Link ATM network is testing a new breed of cash machine capable of accepting desposits for multiple banks.

The first machine is up and running in Atherstone in Warwickshire and further ATMs will also be trialled, according to Cash Access UK.

With the gradual disappearnce of local bank branches from the high street, the new machines will help to alleviate the stresses on small business owners who often have to travel long distances to deposit their cash takings.

The decline of the bank branch network has left many without vital services, in particular the ability for small business owners to deposit takings for the day safely without shutting the small business early or travelling for miles. The ability to deposit in a super-ATM that works for multiple banks is an important innovation and could make a real difference alongside the accelerated rollout of banking hubs and maintenance of Post Office counters.

National chairman of the Federation of Small Businesses (FSB) Martin McTague

Cash in Ireland

Recent proposals for access to cash legislation aim to ensure the continuation of reasonable access to cash for all Irish citizens who wish to, or have a need to, use cash. While as many as 94% of us say we use it, cash is seen as particularly important for the inclusion of vulnerable consumers.

The General Scheme of the Access to Cash Bill 2024 arises from a recommendation of the 2022 Retail Banking Review to put reasonable access to cash on a legislative footing. According to the Review, reasonable access to cash is "the ability to withdraw and deposit notes and coin at locations within a reasonable distance and at a reasonable cost".

The draft legislation focusses primarily on the availability, operation and accessibility of ATM services and cash service points and, if passed, will have important implications for supporting the financial inclusion of consumers.

The legislation seeks to preserve the level of access to cash that prevailed as of December 2022, as recommended by the Retail Banking Review. Some credit unions are independently moving to offer ATM services, using ATM operators to facilitate access to cash in their local communities and motivated by a desire to support financial inclusion.

If it looks and acts like credit

We want Australians to enjoy the benefits of BNPL, while knowing there are strong consumer protections in place. If it looks and acts like credit, then it should be regulated as such.

Assistant Treasurer and Minister for Financial Services, Stephen Jones MP.

Australia's government is prepping legislation that would require buy now, pay later providers to carry out basic credit checks on new customers.

Australia has seen take up of BNPL products from firms such as Afterpay, Klarna and Zip soar in recent years, with around 40% of people using them in the first half of the year, according to a Finder survey.

The government says it recognises the competition that BNPL has brought into the credit markets but notes that most of these products are not currently covered by the National Consumer Credit Act.

To address this, it is planning to amend the act so that providers are required to hold a credit license and comply with existing laws about checks.

However, the legislation will also establish a new category of ‘low‑cost credit’ under the Act "to reflect the lower risk and cost of BNPL compared with other regulated forms of credit".

In brief

Mastercard has launched 'Mastercard for Fintechs', a dedicated programme for startups in Western Europe, offering access to technology support and educational tools alongside a series of fintech events with the opportunity to compete for the chance to win €50,000.

Markus Braun, the disgraced ex-boss of Wirecard, has been forced to rely on state provided legal support after his former lawyer quit because of lack of funds.

Today’s Payments:Unpacked is brought to you by Card Industry Professionals.

Card Industry Professionals believe in providing businesses with a choice when it comes to accepting payments in-store and online, offering a range of propositions, products and plans, to make sure they receive the best solution for their needs.

Find out about the different payment solutions on offer here: Card Industry Professionals | UK Card Payment Solutions

Enhance your payments knowledge